Our Client Service Centre and Hotline will close early at 1pm on Friday, 21 August 2026 for our company event. We apologise for the inconvenience and look forward to serving you when we resume normal operations on Monday, 24 August 2026.

View more

Important Notice

Exercise caution and remain vigilant against scammers posing as Manulife Singapore staff or financial representatives, or government officials.

Manulife Singapore staff and our financial representatives are committed to ensuring your security, and we will:

1. Never call on behalf of the Monetary Authority of Singapore (MAS). 2. Never request money transfers on behalf of MAS. 3. Never ask for money transfers to any bank account over the phone. For payment of premiums, do refer to https://www.manulife.com.sg/en/self-serve/make-payment.html for our official payment channels. 4. Never request for your personal or financial credentials, such as passwords, one-time PINs (OTPs), or security codes, via phone or email.| 5. To view details of your servicing agent, log in to your account via MyManulife or Manulife SG App and navigate to Policies > Policy Information

If you have any doubts or concerns, please contact our hotline at 6833 8188 (available 9am – 5pm, Mon-Fri, excluding public holidays) or submit a form here for assistance.

Our Client Service Centre and Hotline will close early at 1pm on Friday, 21 August 2026 for our company event. We apologise for the inconvenience and look forward to serving you when we resume normal operations on Monday, 24 August 2026.

View more

Important Notice

Exercise caution and remain vigilant against scammers posing as Manulife Singapore staff or financial representatives, or government officials.

Manulife Singapore staff and our financial representatives are committed to ensuring your security, and we will:

1. Never call on behalf of the Monetary Authority of Singapore (MAS). 2. Never request money transfers on behalf of MAS. 3. Never ask for money transfers to any bank account over the phone. For payment of premiums, do refer to https://www.manulife.com.sg/en/self-serve/make-payment.html for our official payment channels. 4. Never request for your personal or financial credentials, such as passwords, one-time PINs (OTPs), or security codes, via phone or email.| 5. To view details of your servicing agent, log in to your account via MyManulife or Manulife SG App and navigate to Policies > Policy Information

If you have any doubts or concerns, please contact our hotline at 6833 8188 (available 9am – 5pm, Mon-Fri, excluding public holidays) or submit a form here for assistance.

We have created this page to help explain some of the key terms related to your insurance policies, making it easier to navigate and understand the terms of the industry better.

Please note that this glossary has been created for informational purposes and should not be considered as legal or financial advice. Contractual terms and conditions will prevail should any of the content in this glossary conflict with your policy documents.

Account value is the prevailing net value of all units under the funds you have invested in your investment-linked policy.

Attained age

This refers to the life insured's age last birthday at any time.

Automatic fund rebalancing

Automatic fund rebalancing allows you to keep your portfolio holdings in line with your investment strategy. When this option is selected, the existing fund holdings will be readjusted at each policy anniversary to achieve the fund split in accordance with the premium allocation.

Automatic Premium Loan (APL)

The insurer will pay the overdue premium amount by deducting the amount from the cash value of the policy. This feature allows you to stay covered even if you have missed a premium payment.

Basic Benefit

This refers to the basic insurance coverage provided by your policy, as outlined in the contract.

Beneficiary

A beneficiary is a person or entity (such as a trust) you have nominated to receive the proceeds of the policy (or the death benefit).

Cash value

Cash value comprises of guaranteed benefits and/or non-guaranteed bonuses that your policy has accumulated over time.

If you decide to cancel (or "surrender") your policy, you will receive this cash value (also known as surrender value). Keep in mind that cancelling your policy early may involve penalty charges, meaning the cash value could be less than the premiums you've paid up to that point.

Coupons

Depending on the features of your policy, cash coupons may be paid out at regular intervals during the policy term, provided that the policy is in force. These coupons are automatically accumulated in your policy. You may request to change your coupon option to either withdraw (payout) or accumulate them within your policy. Refer to your contract for exact terms and conditions.

Cover / Coverage

This is the amount of protection your insurance policy provides.

Before selecting a policy, it's important to discuss your needs with us. Make sure to read the policy's terms and conditions to clearly understand what is covered and what is not.

Critical illness (CI)

The Life Insurance Association Singapore (LIA) provides standard definitions for the severe stage of 37 critical illnesses.

Subject to the terms at the point of application, critical illness insurance pays out a lump sum if the insured is diagnosed with one of the critical illnesses specified in the policy contract.

Before selecting a policy, it's important to discuss your needs with us. Make sure to read the policy's terms and conditions to clearly understand what is covered and what is not.

Death benefit

The death benefit is the amount paid out to your beneficiaries if the life insured passes away while the policy is active and within the policy term.

For details on how the death benefit is calculated, please refer to your policy contract.

Exclusions

Exclusions are specific conditions or situations that are not covered by your insurance policy.

Before selecting a policy, it's important to discuss your needs with us. Make sure to read the policy's terms and conditions to clearly understand what is covered and what is not.

Free-look period

The free-look period allows you to cancel your policy by notifying us in writing within 14 calendar days after you receive the policy.

Grace period (Premium payment)

This is the amount of time during which we continue to provide coverage even if you miss a premium payment. The grace period lasts for 30 calendar days from the premium due date. It is crucial to pay your premium before the grace period ends to maintain your protection.

Guaranteed Cash Benefit (GCB)

Depending on the features of your policy, cash benefits may be paid out at regular intervals during the policy term, provided that the policy is in force. You may request to withdraw the cash benefits (payout), accumulate them within your policy, or use them to pay for premiums that are due. Refer to your contract for exact terms and conditions.

Guaranteed renewal

This means that as long as you continue to pay your policy premiums, we will renew your coverage up to a pre-agreed age or according to the terms specified in your policy contract.

Immediate family member

An immediate family member typically includes a spouse, child, adopted child, stepchild, sibling, or parent.

Incontestability provision

The incontestability provision ensures that, except in cases of fraud, non-payment of premium, or exclusions, we cannot deny a claim due to errors in your policy details after a specified period within the policy term, typically 2 years.

Initial premium

This is the first premium payment made under a new insurance policy.

Insurability

Insurability refers to your eligibility for insurance coverage. We evaluate factors such as health, age, and risk profile before making a decision on coverage.

Investment-linked policy (ILP)

An investment-linked policy (ILP) is an insurance plan that provides both investment opportunities and life insurance coverage. The policy's value depends on the performance of the funds chosen, and it is important to select funds that align with your investment objectives and risk profile.

Issue age

This is the age used as the basis for determining the premium for the life insured when purchasing a policy. It is calculated as your age on your last birthday as of the policy start date.

Lapse

This means that you are no longer covered by your policy. It happens when you stop paying your premium after the grace period or when your policy's cash value is insufficient to pay for the applicable premiums or charges.

Level premium

This is a type of life insurance where premiums stay the same throughout the term of the policy.

Life insured

The person who is covered under an insurance policy.

Life insurance policy

The primary purpose of a life insurance policy is to provide protection, offering financial support in emergencies when the life insured passes away or becomes totally and permanently disabled. Some life insurance products also include an investment component alongside the insurance coverage e.g. investment-linked policies.

Limited pay option

The limited pay option allows you to pay premiums for a set number of years while enjoying the benefits of the policy until the end of its term. This option can be particularly beneficial if you purchase a policy later in life and prefer to limit the period for which you pay premiums.

Loyalty bonus

This is a feature in certain investment-linked policies that rewards your continued commitment to the policy by providing additional units when specific conditions are met. Typically, loyalty bonuses are not guaranteed.

Maturity date

This is the pre-agreed date on which a policy ends. A policy is no longer effective after its maturity date.

Minimum Investment Period (MIP)

The period from policy inception during which a premium shortfall charge, partial withdrawal charge, or surrender charge may be applied. Refer to your contract for exact terms and conditions.

Outstanding loan

The total amount owed to the policy, including accrued interest. This can arise from an Automatic Premium Loan (APL) due to unpaid premiums and/or from policy loans.

Partial withdrawal charge

For some policies with cash values, you may request a partial withdrawal. A partial withdrawal charge may be applied if the withdrawal is made within a certain period. Refer to your policy contract for exact terms and conditions.

Participating policy

A participating policy allows you to share in the profits of the company's participating fund. Your share of the profits is distributed in the form of bonuses or dividends to your policy. These bonuses or dividends are not guaranteed, as they primarily depend on the investment performance of the participating fund.

Payout

Payout includes both guaranteed and non-guaranteed amounts. The frequency of the policy payout is based on your selected schedule or the default option of the plan.

Policy loan

A policy loan allows you to borrow against the cash value of your insurance policy. Interest is charged on the loan, and any unpaid amount will be deducted from the policy's cash value. There are various types of loans available, so we recommend discussing your needs with us first to determine the best option for you.

Policy owner

A policy owner, also known as a policyholder, is the person in whose name the insurance policy is held. If you purchase an insurance policy under your own name, you are the policy owner. As the policy owner, you have the ability to add more people to your policy, making them additional 'people insured' under the policy.

Policy year

This refers to a consecutive 12-month period, starting from the day the policy becomes effective.

Pre-existing condition

A pre-existing condition refers to any medical condition or illness that existed before the policy becomes effective. It is crucial to declare these conditions so we can determine if they can be covered under your policy. Failure to disclose pre-existing conditions upfront may result in your policy becoming invalid.

Premium

This is the amount of money you pay for your insurance policy. Subject to the policy's terms and conditions, it can be paid as a single premium or on a monthly, quarterly, semi-annual, or annual basis.

Premium paying period

This is the length of time during which the policy owner is required to pay regular premiums. This period can vary depending on the type of policy.

Premium rate

The premium rate is the cost of your insurance coverage and may vary from year to year depending on the level of coverage and your risk profile. Some premium rates can be fixed; these are known as "level premiums."

Premium shortfall charge

If you miss a regular basic premium payment for your investment-linked policy, a premium shortfall charge may be applied for the period during which premiums are missed. Refer to your policy contract for exact terms and conditions.

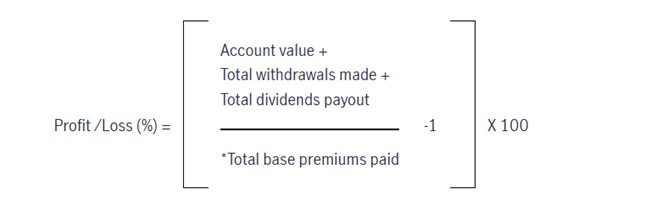

Profit/Loss (%)

In investment-linked policies (ILP), the Profit/Loss percentage (%) reflects how the investment is performing compared to the total base premiums paid.

It is calculated using this formula:

*Please note that the total base premiums exclude any premiums for supplementary benefits and riders, as these do not contribute to the investment performance of the policy.

Profit/Loss amount

For investment-linked policies (ILP), the Profit/Loss amount is derived from the Profit/Loss percentage (%) explained above.

The Profit/Loss amount is calculated by multiplying the Profit/Loss percentage (%) by the total base premiums paid, including any top-ups made to the policy.

Rider

Also known as a supplementary benefit, a rider is an additional benefit that a policy owner can purchase to enhance a life insurance policy. Adding a rider increases the level of your coverage and typically results in higher premiums.

Risk profile

Your risk profile indicates the amount of investment risk you are willing to bear. It varies from individual to individual and can change over time as you age, and as your financial situation and investment objectives evolve.

Surrender

Surrender refers to the cancellation of an insurance policy.

Surrender charge

For some policies, there may be a charge imposed upon the full surrender of the policy. This charge will be deducted from the total account value of the policy to determine the surrender value of the policy. Refer to your policy contract for exact terms and conditions.

Surrender value/Net surrender value

The amount payable after deducting any surrender charge and/or outstanding loans (if applicable). For investment-linked policies, the actual surrender value depends on the applicable unit price at the time the fund(s) are sold.

Term life insurance

Term life insurance provides coverage for a fixed period of time. It offers a death benefit to the beneficiaries if the life insured passes away during the term of the policy.

Total account value

The value of your investment in any or all the funds you own. This is equal to the number of units you own multiplied by the unit price of the fund.

As such, the total account value is the gross total value computed by summing all the respective fund units multiplied by the latest fund price.

Total available loan

The maximum amount that can be borrowed from the policy, using the policy's cash value as collateral.

Total premium paid to date

This reflects the total premium paid, including waived premiums, premium offset by Guaranteed Cash Benefit (GCB), policy discounts, top-ups, and Automatic Premium Loan (APL) since policy inception.

Valuation day

This is the date on which units in your investment-linked policy are bought or sold on your behalf, determining the value of the units. This date may vary from fund to fund and can be affected by fund holidays or any pending transactions, including monthiversary processing.

Whole life insurance

Whole life insurance provides lifelong protection and is available in different forms, such as participating and non-participating policies. It offers a death benefit, with most products also covering total and permanent disability, and some products covering major illnesses.