This content was contributed by Manulife Investment Management (Singapore) Pte. Ltd

WealthStyles (investor education series) – Take one step closer in achieving your life goals through portfolio construction

01 October 2020 | 5-mins read

Whether you’re getting married in three to five years’ time, or preparing for a comfortable retirement 30 to 40 years later, it makes sense to grow your savings through a sound financial plan over time. This way, you are better-placed to achieve the desired amount over the target timeframe.

While it may be tempting to dabble in equities, or trade in forex with hopes to make an easy return, they are neither effective nor systematic ways to manage your money. This is especially true when investing over a long period or during periods of economic uncertainty.

To be a step closer in achieving your goals, you may need to construct a portfolio that takes into account asset allocation, risk management and capital appreciation.

Generally speaking, portfolios can be classified into three types – growth, balanced and conservative. The difference between the three lies mainly in the proportion of risk assets (e.g. equities) in the portfolio.

Equities are potentially more volatile. Generally, the higher the proportion of equities in the portfolio, the higher the potential gains (or losses). For the sake of simplicity, we shall focus our discussion on equities and bonds.

What are the key types of portfolios?

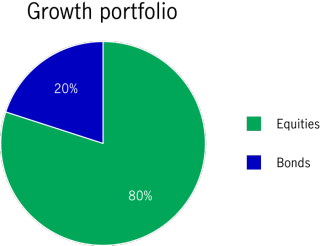

Growth portfolio: The key objective of this portfolio is to achieve long-term capital appreciation. To maximise potential returns, assets are allocated mainly into equities, usually of a proportion between 60% and 100%. It is suitable for investors who are more aggressive and have a higher risk tolerance.

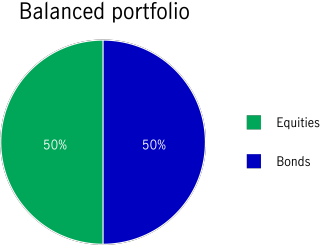

Balanced portfolio: With a goal of achieving balanced long-term capital appreciation, asset allocation is not concentrated on just equities or a single asset class. Instead, instruments with lower volatility (such as investment grade bond funds with regular income distribution features, exchange-traded funds (ETFs), money market funds and cash deposits) are used to balance the overall volatility of the portfolio. It is therefore suitable for investors who can tolerate a medium level of risk, and are aiming to strike a balance between risks and returns.

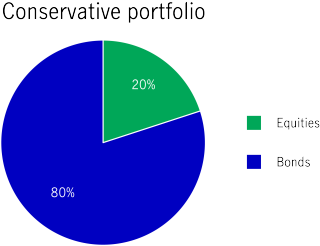

Conservative portfolio: The objective of this portfolio is to seek steady growth and control downside risks. With stability as a key focus, this portfolio type holds a smaller proportion of equities, typically not exceeding 20% to 30%, so as to minimise volatility. Conservative portfolios are suitable for investors who are more conservative and cannot tolerate large investment losses.

Asset ratios in the three aforementioned portfolios are for reference only. These classifications are not standardised; the risk profile of a portfolio depends largely on the largest asset class in the portfolio.

How have these portfolios performed in the past?

An investor’s investment horizon is different at various life stages, ranging from anything between 3-5 years and 30-40 years. It can also span multiple economic cycles. As shown in the table below, portfolios with a higher proportion of bonds can buffer downside during economic downturns. In other words, it potentially helps investors to better manage downside risks.

However, when the economy recovers, equities tend to outperform bonds due to better corporate earnings, improved corporate and consumer confidence, as well as higher risk appetite in investment markets. As a result, equity markets attract more capital inflows. In this part of the market cycle, the overall return is higher for portfolios with a greater proportion of equities.

Looking at the performance of the MSCI World Total Return (USD) Index and Bloomberg Barclays Global Aggregate Bond Index (USD hedged), the value of growth portfolios rose more than 160% in the last economic upcycle; balanced portfolios holding equal proportions of equities and bonds rose slightly less (approximately 120%) while conservative portfolios with only 20% of equity holdings gained 83%.

Yet when the economy is not doing well, equities often perform worse than bonds and this in turn drags down the portfolio’s overall performance. Growth portfolios lost nearly 30% in the last economic downturn; balanced portfolios, with 30 percentage points more bond holdings than growth portfolios, fell less (approximately 16%) while conservative portfolios with almost 80% holdings in bonds fell around 2%.

How should investors start constructing their investment portfolios?

There are two ways to construct a portfolio:

Multi-asset funds: These funds make flexible allocations across different asset classes, adjusting for factors such as investment objectives and market risks. These portfolios are usually made up of dozens of holdings, offering growth, balanced and conservative options, or different options for various retirement objectives, with a range of equity-to-bond ratios for investors to choose from.

Another type of multi-asset fund is “fund-of-funds”, which invests into other funds. By investing in a basket of funds, it may hold up to hundreds of securities, which further helps to diversify risks.

Self-constructed portfolio: Investors may also choose to construct their own portfolios by buying different asset classes directly through personal investment accounts. The investor handles the entire process, from screening and trading to asset allocation.

Comparing the two options, the first option is managed by professionals. Therefore, it saves investors the hassle of figuring out the right combination of holdings. It also holds a scale advantage and some of the funds offer access to investment tools used by global retail and institutional investors. This option is relatively easier than managing a portfolio on your own.

If you have any questions about portfolio construction, or any specific requirements, please speak with your financial advisor.

1 Source: Bloomberg, as of 30 June, 2020. Total returns in USD. Equities are represented by MSCI World Total Return (USD) Index; while bonds are represented by Bloomberg Barclays Global Aggregate Bond Index (USD hedged), assuming monthly rebalancing for each portfolio. The periods of economic cycles were based on the US economic cycle stated by the US National Bureau of Economic Research. Past performance is not indicative of future performance. The information above is for reference only. Investors cannot invest directly in an index.

2 Preferred securities are fixed-income instruments with equity-like features.

This material was prepared solely for informational purposes and does not constitute a recommendation, professional advice, an offer, solicitation or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security. This material should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell any investment products or to adopt any investment strategy. Nothing in this material constitutes investment, legal, accounting or tax advice, or a representation that any investment or strategy is suitable or appropriate to your individual circumstances, or otherwise constitutes a personal recommendation to you. Past performance is not an indication of future results.

Important note:

The information provided on this website is for informational purposes only and is intended solely for use by Singapore residents and is not intended for distribution to, or use by, any person or entity in the United States, or any jurisdiction or country where such distribution or use would be contrary to law or regulation, or which would subject Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G), Manulife (Singapore) Pte. Ltd. (Company Registration No. 198002116D) and/or its affiliates (collectively hereafter "Manulife") or any of Manulife's products or services to any registration requirement within such jurisdiction or country. Nothing on this website shall be construed as financial advice or an offer, invitation, solicitation or recommendation by or on behalf of Manulife to any person to buy or sell any Fund and is no indication of trading intent in any Fund managed by Manulife. None of the information or analyses presented are intended to form the basis for any investment decision, and no specific recommendations are intended. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Thank you for contacting Manulife Singapore!

Our Financial Consultant will be in touch with you soon.

Here are some links you might find useful.

Consent

By submitting your personal details,

- You acknowledge that you authorise and consent to Manulife (Singapore) Pte Ltd ("Manulife) (including employees and Representatives of Manulife) to collect, use, disclose and retain your personal data for the purpose of receiving notifications via SMS(es) and email(s) to service your request; and

- You consent to Manulife to contact you (even though your telephone number may be already registered on the National Do Not Call Registry) for marketing purposes, and to provide you with marketing, advertising and promotional information, materials and/or documents relating to financial advisory services and products distributed by Manulife, if applicable.

The consent you provide is in addition to and does not supersede, vary or nullify any consent which you may have provided previously in respect of the above purposes, unless your previous consent has been withdrawn.

You also confirm that you are the user and/or subscriber of the telephone number and email address provided by you.

More Insights you might find interesting

How to invest your savings at every age.

What is an Investment-Linked Policy (ILP) and is it suitable for me?