This content was contributed by Manulife Investment Management (Singapore) Pte. Ltd

Bank failures—unexpected events make investment decisions difficult

31 March 2023 | 3-mins read

The market volatility unfolding after the recent events in the U.S. and European banking sectors is raising many questions in the minds of investors as to what they should do with their investments. Our Capital Markets and Strategy Team in the Macroeconomic Strategy Group takes a step back and looks at what has happened over the course of the last few years and how we might frame discussions with those skittish investors.

Q1: What’s the background behind the recent market volatility?

Interest rates increased after COVID. Approximately three years ago, the global COVID-19 pandemic was born. Since that time, we’ve had entire countries shut down, globally distributed vaccines, restrictions to cross-border travel, and an eventual gradual reopening. In an effort to minimize the economic impact of the shutdowns, governments around the world provided trillions of dollars in support through federal subsidies and low interest rates.

With an excess of money in the system and an imbalance between supply and demand of goods and services, inflation rose globally to levels not seen in decades. Once the various countries reopened and economies were on solid footing, central banks shifted their focus to reducing inflation. Global central banks began to raise interest rates, some more aggressively than others.

A sizeable increase in interest rates, predominantly in North America, has exposed some individuals and companies who may not be able to weather higher costs during a slowing economy. Many of us know at least one person who has felt the stress from rising interest rates, perhaps from an increase in monthly mortgage costs. Companies are no different, and to varying degrees, they’ve also felt the stress of rising interest rates.

Q2: Will we experience more volatility in the short-term?

Bank failures added to uncertainty. Most recently, market volatility ensued on the signs of trouble in the U.S. and European banking sectors. In the short term, we’re likely to experience more volatility as the market digests the ongoing fallout from regional banks and potential swings in prices in other areas of the market. As the global economy digests the interest rate hikes from last year, we believe U.S. inflation will continue to trend lower (our view is 4% by the end of the year). And should that be the case, central banks such as the U.S. Federal Reserve, are likely getting close to ending their rate hike cycle, if they’re not already there. In fact, headline inflation has started to decline in most emerging market economies in Asia.1 Many central banks in the Asia region have already made a dovish pivot—for example, Thailand and Vietnam.2

Any market volatility tends to cause the same uneasy feeling for investors, and they start to question their investment choices.

Q3: Why is it hard to make the right financial choices in difficult times?

It’s not always easy to make wise investment decisions, and this is especially true during uncertain times. When we’re stressed, we tend to make choices more intuitively and are less likely to spend time carefully sifting through all the pros and cons. The trouble is that intuitive snap decisions won’t necessarily help us meet our long-term financial goals.

Daily availability to market commentary and data has likely shortened investors’ timeframes, as we’re more prone to have knee-jerk reactions to short-term events. As humans, we naturally have biases that we must overcome (such as loss aversion, where the pain of losing is psychologically more powerful than the pleasure of gaining).

We can likely all agree that we shouldn’t react to short-term events and make changes to investments that were based on our long-term plans. Our time frame for our long-term goals is likely to change depending on the stages of our lives. And while there are no guarantees, at its core, investing is trying to make decisions to increase your odds of success.

Q4: How should we approach our investments? Should we take a short-term, or medium to long-term view?

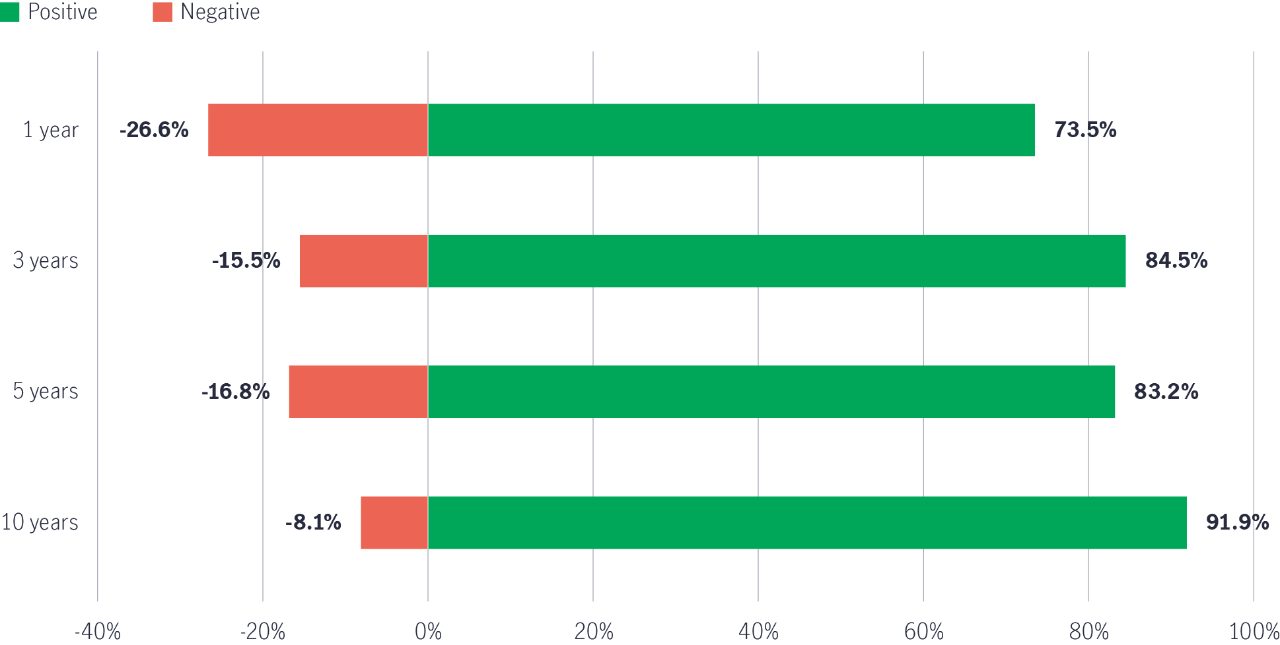

As the chart below illustrates, having a time frame of greater than three years increases those odds. The table shows returns and odds of being positive for four different time frames: 1, 3, 5, and 10 years (Chart 1).

Chart 1: Markets are positive more often than negative

S&P 500 price index (odds of being positive vs. negative) – since 1950

Source: Bloomberg, Manulife Investment Management, Capital Markets Strategy. As of March 31, 2023.

Source: Bloomberg, Manulife Investment Management, Capital Markets Strategy. As of March 31, 2023.

Three main points to note:

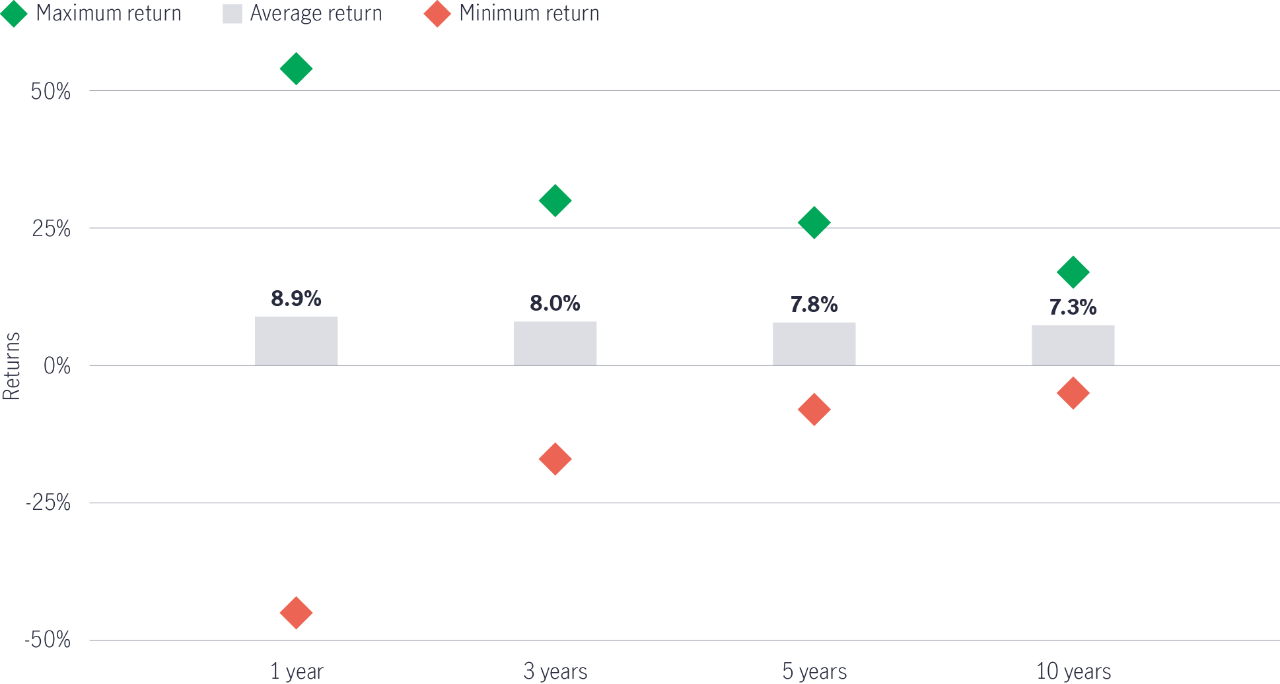

- Over the short term (1 year), the average return was highest but the range in returns was by far the widest. (Chart 2) A maximum return of 54% to a minimum return of -45%. Markets are volatile in the short term and the odds of being positive are only 74%.

- Over the long term (10 years), the average return was the lowest at 7.3%. However, the range in returns was small. A maximum return of 17% to a negative return of -5%, with the odds of being positive at 92%.

- Over the medium term (3-5 years), returns were approximately 8% with the shorter three-year term having a wider range. The odds of being positive are approximately 85%.

Chart 2: Longer time frame leads to less variability in returns

S&P 500 index historical returns based on time frame (since 1950)

Source: Bloomberg, Manulife Investment Management, Capital Markets Strategy. As of March 31, 2023.

Source: Bloomberg, Manulife Investment Management, Capital Markets Strategy. As of March 31, 2023.

The results of the historical data are clear: markets are much more volatile in the short term with big movements to both the upside and downside. But typically, over the medium to long term, the odds are in investors’ favour of both a positive return and one that’s likely to help them reach their financial goals. Perhaps this quote best captures the essence of how we should approach our investments during periods of short-term volatility:

“Investing is like soap: the more you touch it, the smaller it gets.”

1 Manulife Investment Management, Q1 2023 Global Macro Outlook: The year ahead

2 Manulife Investment Management, Assessing the contagion risk from ongoing banking concerns to Asia, 21 March 2023

Important note:

The information provided on this website is for informational purposes only and is intended solely for use by Singapore residents and is not intended for distribution to, or use by, any person or entity in the United States, or any jurisdiction or country where such distribution or use would be contrary to law or regulation, or which would subject Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G), Manulife (Singapore) Pte. Ltd. (Company Registration No. 198002116D) and/or its affiliates (collectively hereafter "Manulife") or any of Manulife's products or services to any registration requirement within such jurisdiction or country. Nothing on this website shall be construed as financial advice or an offer, invitation, solicitation or recommendation by or on behalf of Manulife to any person to buy or sell any Fund and is no indication of trading intent in any Fund managed by Manulife. None of the information or analyses presented are intended to form the basis for any investment decision, and no specific recommendations are intended. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Thank you for contacting Manulife Singapore!

Our Financial Consultant will be in touch with you soon.

Here are some links you might find useful.

Consent

By submitting your personal details,

- You acknowledge that you authorise and consent to Manulife (Singapore) Pte Ltd ("Manulife) (including employees and Representatives of Manulife) to collect, use, disclose and retain your personal data for the purpose of receiving notifications via SMS(es) and email(s) to service your request; and

- You consent to Manulife to contact you (even though your telephone number may be already registered on the National Do Not Call Registry) for marketing purposes, and to provide you with marketing, advertising and promotional information, materials and/or documents relating to financial advisory services and products distributed by Manulife, if applicable.

The consent you provide is in addition to and does not supersede, vary or nullify any consent which you may have provided previously in respect of the above purposes, unless your previous consent has been withdrawn.

You also confirm that you are the user and/or subscriber of the telephone number and email address provided by you.

More Insights you might find interesting

How to invest your savings at every age.

What is an Investment-Linked Policy (ILP) and is it suitable for me?