What are your options if you cannot afford premium payments?

31 March 2023 | 2-mins read

Supporting our customers who are facing financial difficulties is important to us. There are various options you can choose from if you are having difficulties paying your premiums, without forfeiting the entire value of your policy.

These options are referred to as Non-forfeiture Options (NFO). They are listed below and they vary across different types of policies. Please refer to your policy contract to find out which options are applicable to you.

- Non-forfeiture Option 1: Automatic Premium Loan (APL)

- Non-forfeiture Option 2: Reduced Paid-up

- Non-forfeiture Option 3: Reduce Sum Insured

- Non-forfeiture Option 4: Premium Holiday

- Non-forfeiture Option 5: Premium Freeze

This is a simple guide on the types of NFO that are made available under your policy contract. This guide is for general information purpose only. It is not intended to provide or constitute specific financial, tax, legal, investment or any other advice. Please consult your Financial Representative to conduct a holistic review on your insurance portfolio before deciding on an option that best fits your financial need.

Here is a quick overview of each option, and the category of customers who may suit the specific option.

| Non-forfeiture Option | Customers who may suit this option |

Automatic Premium Loan (APL) |

Customers who require temporary financial assistance and wish to keep a large part of the protection coverage intact, and do not have an immediate need to withdraw any cash value from the policy. The policy cash value must be sufficient to support the overdue premium amount and accrued interest for the temporary period. |

Reduced Paid-up |

Customers who decide to cease future premium payments, and do not have an immediate need to withdraw any cash value from the policy. These customers also do not require the full protection coverage, and do not mind giving up the supplementary benefits attached to the policy. |

Reduce Sum Insured |

Customers who foresee an extended period of financial difficulties and are only able to pay smaller premium amount in the near future; or would prefer to receive some cash value payout from the policy. |

Premium Holiday |

Customers who require temporary financial assistance and are prepared to incur premium shortfall charges which are more costly in the early years of the policy term. |

Premium Freeze |

Customers who require temporary financial assistance and are comfortable with the delay of the policy maturity or income payout year. |

Non-forfeiture Option #1: Automatic Premium Loan (APL)

How it works

- Automatic Premium Loan (APL) enables the insurer to pay the overdue premium amount on your behalf, by advancing the cash value of the policy as a loan.

- Interest is chargeable on the APL amount, based on the interest rate determined by insurer from time to time. The current interest rate charged by Manulife (Singapore) Pte. Ltd. (Manulife) for policies denominated in Singapore dollar is 6.75% per annum.

- This APL feature is a default NFO for some participating policies, which automatically takes effect if you do not pay each overdue premium after the end of grace period stated under the policy contract.

- This feature is also dependent on whether the policy has accumulated sufficient cash value to support the overdue premium amount and accrued interest.

- Accumulated APL amount, accrued interest and other deductions stated under the policy contract will be fully deducted from the policy proceeds, such as the surrender benefit, maturity benefit or claim payout (where applicable).

- Please refer to your policy contract for terms on APL.

Example:

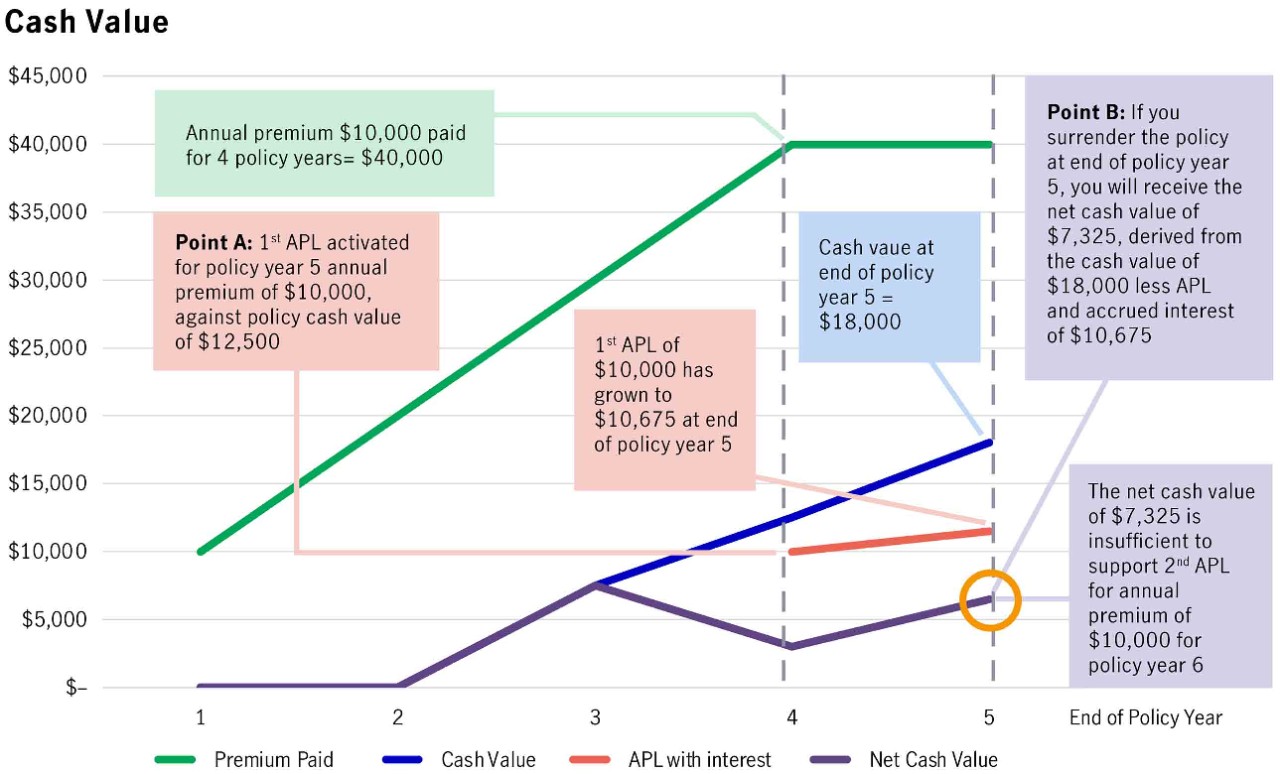

After paying annual premiums for 4 policy years, you are unable to pay the overdue annual premium amount for the 5th policy year after the end of the grace period, the APL automatically takes effect, if there is sufficient cash value under the policy to support this APL option (see Point A in chart below).

In the following year, with the APL still in effect, the policy cash value is unable to support the payment for the 6th annual premium. If you decide to surrender the policy at this point, you will receive the net surrender value, less the accumulated APL amount, accrued interest, and other deductions stated under the policy (see Point B in chart below).

Note: This chart is for illustration purpose only and does not depict the actual policy value or cash value.

Note: This chart is for illustration purpose only and does not depict the actual policy value or cash value.

How is the sum insured or protection benefit of your policy impacted?

- The APL feature does not change the sum insured of your policy. Upon any claim, the insurer will pay the insured benefit, less accumulated APL amount, accrued interest, and other deductions stated under your policy contract.

Is this option suitable for you?

- It is important to note that the interest charged may deplete the cash value of the policy fairly quick. When the policy loan (including APL) and accrued interest amount exceeds the cash value of the policy or policy value, the policy will automatically terminate, and all benefits and coverage will cease on, and from the termination date.

- This option may be suitable if you require temporary financial assistance and wish to keep a large part of the protection coverage intact, and do not have an immediate need to withdraw any cash value from the policy.

- Do keep track of your policy cash value regularly to ensure that there is sufficient cash value to support the overdue premium amount and accrued interest. You should assess how long your policy cash value can sustain the APL. You can contact Manulife Client Services team at service@manulife.com to obtain the latest projected cash value to make this assessment.

- You should try to repay this loan and accrued interest as early as possible in order to manage the increasing interest. You may do so by fully or partially repaying the policy loan (including APL) and accrued interest at any point in time as there is no scheduled repayment program. Once the policy loan (including APL) and accrued interest have been fully repaid to the insurer, the policy will be restored to its original terms.

Nonforfeiture Option #2: Reduced Paid-up

How it works

- Choosing this option means that the cash value of the policy is being used to purchase the policy at a reduced sum insured (i.e. “paid-up” policy).

- While this option will reduce your policy sum insured, it will retain the protection coverage period.

- The policy cash value will continue to grow throughout the policy term but at a reduced rate. You do not need to pay any future premiums.

- Any supplementary benefits attached to the policy will be terminated, and the policy will not be entitled to any future bonus declarations.

- For policy provides a regular income payout, the income payout may either cease or the amount may be reduced.

- Please refer to your policy contract for terms on Reduced Paid-up.

Example:

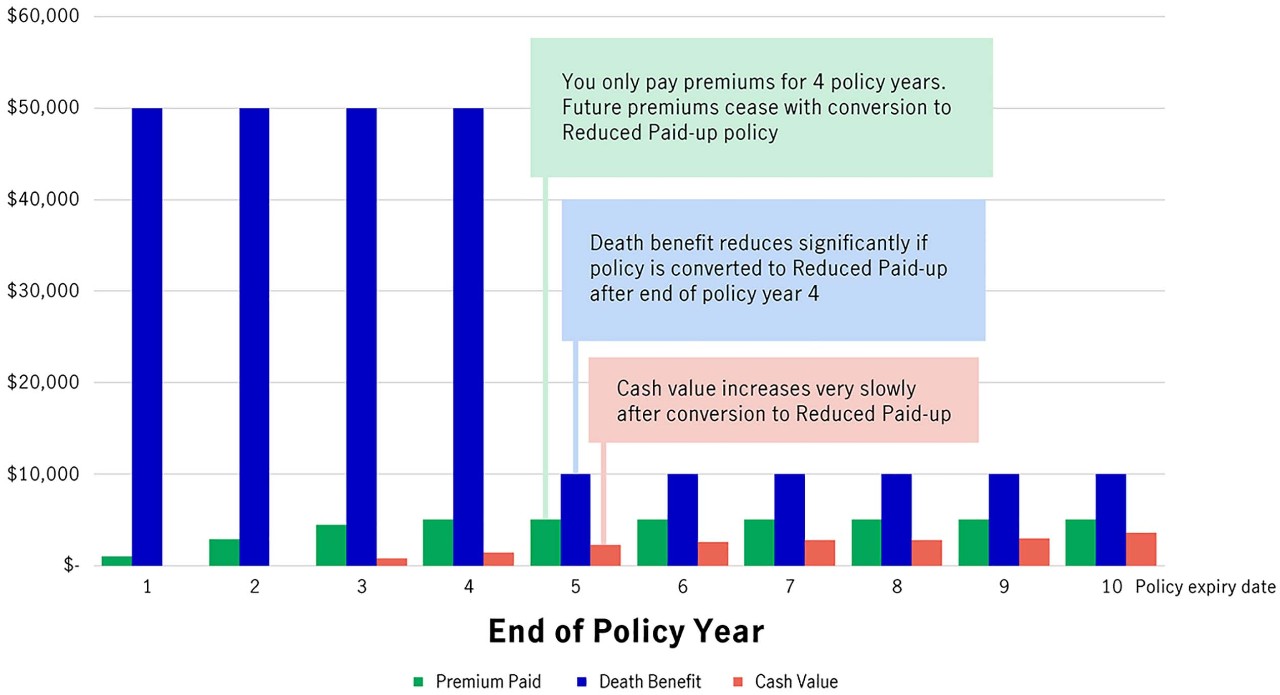

You bought a policy with a policy term and premium payment term of 10 years. After paying premiums for 4 policy years, you decide to convert the policy to a Reduced Paid-up policy. With this option, the death benefit would be adjusted to a reduced amount, while the policy continues to be in force throughout the policy term of 10 years.

Note: This chart is for illustration purpose only and does not depict actual policy value or cash value.

Note: This chart is for illustration purpose only and does not depict actual policy value or cash value.

How is the sum insured or protection benefit of your policy impacted?

- For policy provides a significant protection element in contrast to savings element, the Reduced Paid-up feature could potentially reduce the sum insured by a significant amount, as determined by Manulife.

- If this option is available for your policy, Manulife can calculate the reduced sum insured amount for you before you make a decision. Please contact your Financial Representative or Manulife Client Services team at service@manulife.com if you require more information on the Reduced Paid-up feature or reduced sum insured amount.

Is this option suitable for you?

- This option may be suitable if you have decided to cease future premium payments, and do not have an immediate need to withdraw any cash value from the policy.

- This option would not be suitable if you require the full protection coverage, along with the supplementary benefits attached to the policy.

- It is important to note that once the policy is converted to a Reduced Paid-up policy, you cannot restore the policy back to its original terms in the future.

Nonforfeiture Option #3: Reduce Sum Insured

How it works

- You can choose to tap on the cash value of the policy by reducing its sum insured. This is also known as making a partial withdrawal. Choosing this option means that you will be giving up a part of the policy.

- A partial withdrawal will reduce the sum insured, cash value and benefits under the policy, regardless of the total premiums paid.

- Please refer to your policy contract for terms on Partial Withdrawal.

Example:

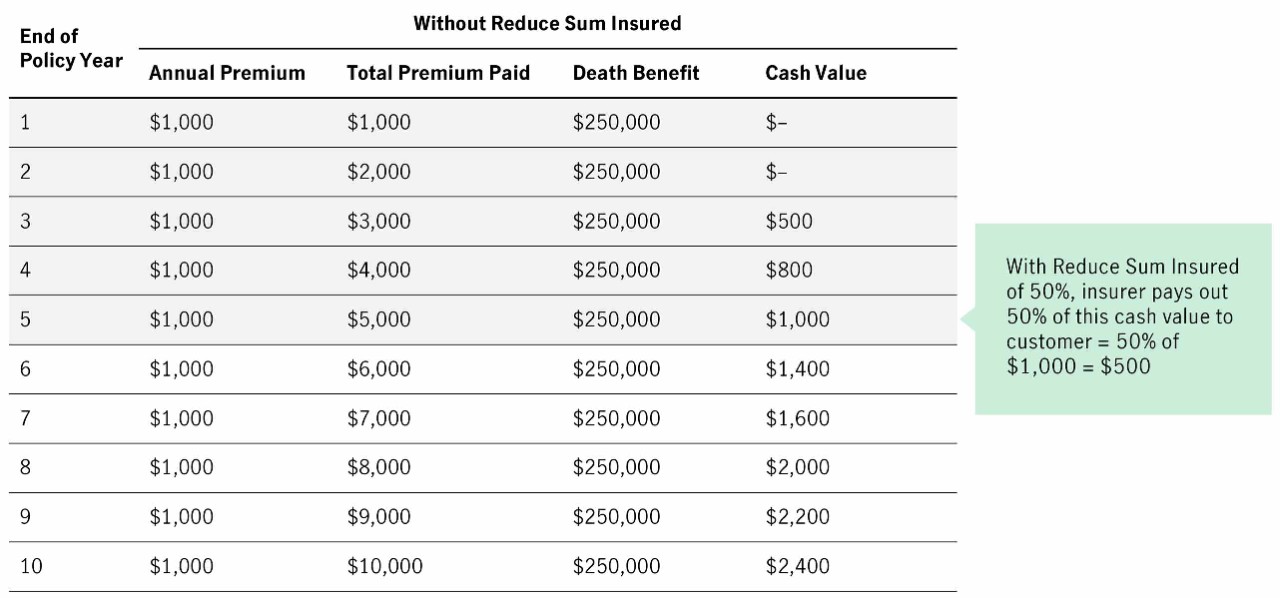

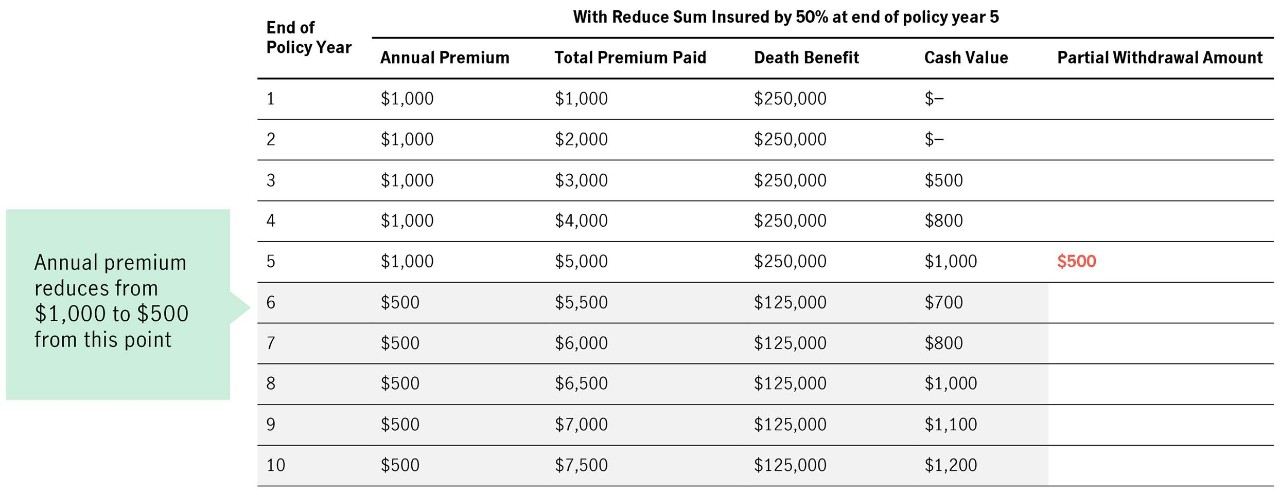

Your policy sum insured is the same as the death benefit of $250,000. You had paid annual premiums for the first 5 policy years at $1,000 per annum (total premium amount paid was $5,000).

At the end of policy year 5, the cash value is $1,000, which is less than the total premiums paid thus far. If you decide to make a partial withdrawal of 50% of the policy, the insurer will pay out 50% of the cash value which amounts to $500.

From this point onwards, the sum insured of the policy will also be reduced by 50% from $250,000 to $125,000, and the cash value will be equally reduced by 50%.

Note: This table is for illustration purpose only and does not depict actual policy value or cash value.

Note: This table is for illustration purpose only and does not depict actual policy value or cash value.

Note: This table is for illustration purpose only and does not depict actual policy value or cash value.

Note: This table is for illustration purpose only and does not depict actual policy value or cash value.

How is the sum insured or protection benefit of your policy impacted?

- The sum insured of the policy will be reduced proportionately by the sum insured portion given up.

Is this option suitable for you?

- This option may be suitable if you foresee an extended period of financial difficulties, and unable to continue paying the originally committed premium amounts in the near future or would prefer to receive some cash value payout from the policy.

- Taking cash out of the policy would impact the policy value, sum insured and benefits under the policy, meaning that the eventual payout amount will be lower than the original terms.

- It is important to note that once there is a partial withdrawal under the policy, you cannot restore the policy back to its original terms in the future.

Nonforfeiture Option #4: Premium Holiday

How it works

- Some investment-linked policies (ILPs) offer a Premium Holiday feature which allows for a temporary stop to premium payment for a stipulated period.

- This feature is usually the default NFO for ILPs, which automatically takes effect if the overdue premiums remain unpaid after the end of grace period stated under the policy contract.

- Insurer may impose Premium Shortfall charge upon activation of this feature, that is deducted monthly against the fund units of the policy.

- Please refer to your Policy Contract for terms on Premium Holiday.

How is the sum insured or protection benefit of your policy impacted?

- The protection benefit for ILP is usually based on a percentage of the premiums paid, sum insured, or account value of the policy, where applicable.

- For policies where the protection benefit is based on the percentage of the premiums paid, the protection benefit will be reduced if the Premium Holiday feature is activated.

- For policies where the protection benefit is based on the sum insured, there will be no change to the protection benefit as long as the policy has sufficient fund units to keep it in force.

Example:

You had paid annual premiums for the first 5 policy years at $10,000 per annum (total premium amount paid was $50,000), and the protection benefit for your policy is 101% of the premiums paid. This amounts the protection benefit to $50,500.

If you had missed 1 year of annual premiums, the total premiums paid would amount to $40,000, and the protection benefit will be $40,400 instead (101% of the $40,000 premiums paid).

Is this option suitable for you?

- It is important to note that the Premium Shortfall charge may deplete the fund units fairly quick. When the net value of the fund units is insufficient to support the policy, the policy will automatically terminate, and all benefits and coverage will cease on, and from the termination date.

- Premium Shortfall charges are more costly in the early years of the policy term and decline in subsequent years. Please refer to the Policy Contract for terms.

- This option may be suitable if you require temporary financial assistance. It will automatically deactivate once premium payment resumes.

- Once this feature is activated, any supplementary benefits attached to the policy will automatically terminate. Policy owner can request to reinstate the supplementary benefits within the reinstatement period upon premium payment but will be required to provide evidence of good health and subject to insurer’s approval.

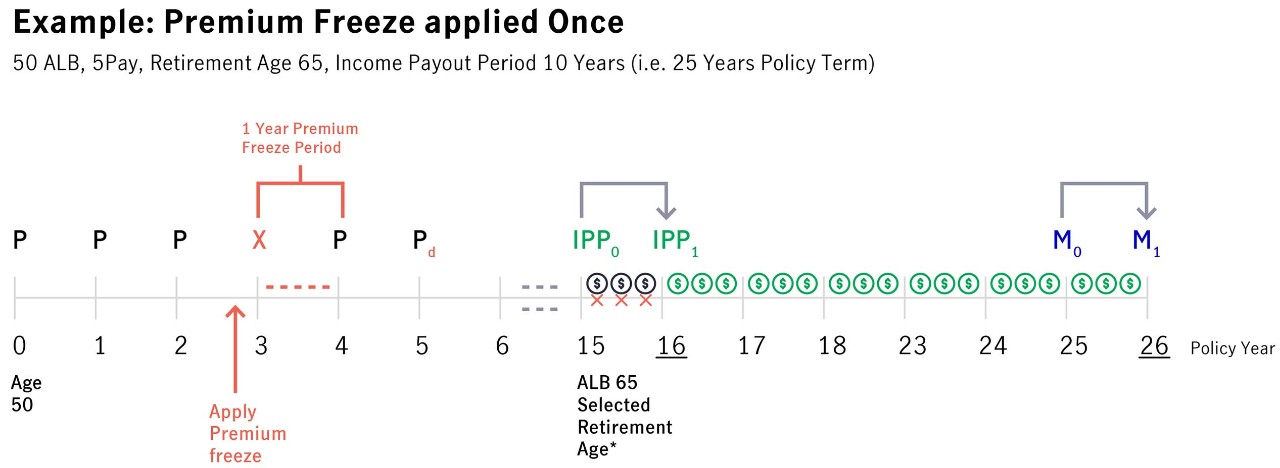

Nonforfeiture Option #5: Premium Freeze

How it works

- A Premium Freeze option enable you to temporarily stop premium payments for one year, starting from the policy’s next premium due date.

- This option will defer the policy maturity date or income payout by 1 year.

- During the Premium Freeze period, the policy will not be entitled to any reversionary bonus declarations or yearly income payouts.

- Typically, insurers would limit this option availability to one or three times, depending on the policy premium payment term.

- Please refer to your policy contract for terms on Premium Freeze.

How is the sum insured or protection benefit of your policy impacted?

- The protection benefit for policies that offer this option is usually based on a percentage of the premiums paid. The protection benefit will be reduced depending on the number of times the Premium Freeze option is activated.

Example:

You had paid annual premiums for the first 5 policy years at $10,000 per annum (total premium amount paid was $50,000), and the protection benefit for your policy is 101% of the premiums paid. This amounts the protection benefit to $50,500.

If you had missed 1 year of annual premiums, the total premiums paid would amount to $40,000, and the protection benefit will be $40,400 instead (101% of the $40,000 premiums paid).

Is this option suitable for you?

- This option may be suitable if you require temporary financial assistance and are comfortable with the delay of the policy maturity or income payout year.

- There is no charge imposed for activating the Premium Freeze option.

ALB Age last birthday

P Premium payable

X No premium paid

...... Premium freeze period

Pd Deferred premium end date due to premium freeze

IPP0 Original start date of yearly income payouts

IPP1 Revised start date of yearly income payouts due to premium freeze

M0 Original maturity date

M1 Revised maturity date due to premium freeze

$ Yearly income payout

More Insights you might find interesting

5 things to know before meeting your Financial Representative

Understanding Insurance Policies: Beat the fine print in insurance