This content was contributed by Manulife Investment Management (Singapore) Pte. Ltd

Why invest in alternative investments now

07 August 2023 | 3-mins read

John Hancock Investment, a company of Manulife Investment Management.

Accommodative monetary policy fueled 60/40 stock-bond investor portfolios for over a decade. Now, shifting conditions point to a new macroeconomic regime that strengthens the case for alternative investment allocations.

Key takeaways

- The period 2012 to 2021 produced historically high Sharpe ratios for 60/40 stock-bond portfolios.

- In a potentially new macroeconomic regime, a 60/40 portfolio faces a combination of challenges.

- Amid higher market volatility and more pronounced business cycles, alternative strategies have the ability to add value within diversified portfolios.

In the wake of the global financial crisis, the U.S. Federal Reserve reduced interest rates to near zero and engaged in massive monetary stimulus programs leading to over a decade of ultra-accommodative monetary policy. The COVID-19 pandemic necessitated the continuation of monetary stimulus measures through 2021. This environment was a boon to risk assets: Benefiting from low interest rates and ample liquidity, investors exhibited a willingness to assume risk and were duly rewarded.

From 2009 to 2021, the S&P 500 Index returned an annualized 16%1, reaching all-time highs and far outpacing its long-term historical average of 9.9%2 and, amid declining interest rates, bond returns were stable, returning almost 4% annually over the same period. More importantly, the environment of easy money precipitated prolonged periods of low-volatility regimes for both equities and bonds; consequently, 60/40 stock-bond portfolios experienced historically elevated risk-adjusted returns. An analysis over rolling 10-year periods from 1989 to 2023 shows a recent period of sustained high Sharpe ratios for a 60/40 portfolio, culminating in 2019 delivering the highest risk-adjusted returns in over 40 years.3

Unprecedented high Sharpe ratios for a 60/40 stock-bond portfolio

Rolling 10-year Sharpe ratio, December 1989–April 2023

Source: John Hancock Investment Management, 2023. 60/40 portfolio is represented by 60% S&P 500 Index and 40% Bloomberg U.S. Aggregate Bond Index. It is not possible to invest directly in an index. Past performance does not guarantee future results.

Against this backdrop of sustained lower volatility and massive monetary stimulus that contributed to historically high risk-adjusted returns for equities and bonds, most alternative strategies were limited in their ability to make a positive impact on portfolios; in fact, allocating away from stocks and bonds into alternatives may have detracted from risk-adjusted performance during this period.

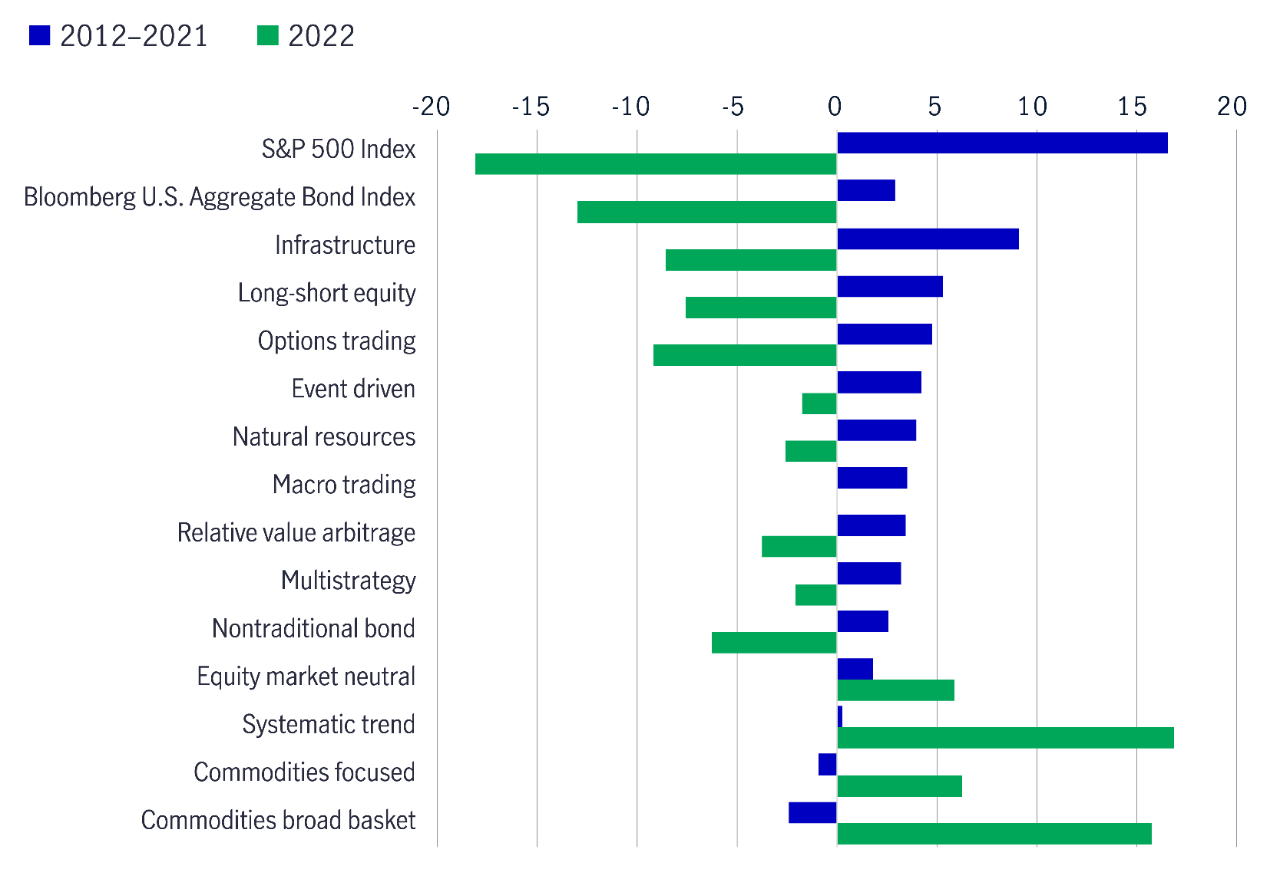

From 2012 to 2021, many alternative strategies posted decent results but were outshined by the stellar risk-adjusted returns from stocks and bonds. In 2022, the economic backdrop that had supported high risk-adjusted equity and fixed-income returns shifted significantly as high inflation became entrenched, resulting in the most aggressive monetary policy tightening cycle in decades. Bonds, which would typically help to cushion portfolios during an equity market correction, declined sharply. Some alternative strategies not only helped to cushion downside performance, but even posted strong positive returns, playing the role of defense in portfolios when bonds couldn't.

Returns of stocks, bonds, and alternative strategies

Source: Morningstar Direct, John Hancock Investment Management, 2023. It is not possible to invest directly in an index. Past performance does not guarantee future results.

The radically altered economic backdrop caused many to question the effectiveness of the traditional 60/40 portfolio while possibly ushering in a new macroeconomic regime for markets.

A new macroeconomic regime paves the way for alternatives

Ascertaining the macroeconomic path ahead for markets is key to understanding how alternative strategies may improve a diversified portfolio. While uncertainty persists around the precise macro outlook, or the path of getting there, most market participants agree that it's unlikely to be a seamless and wholesale return to the ultra-accommodative monetary policy that preceded 2022. This effectively eliminates some of the key monetary policy factors that supported traditional equities and fixed income, and it's expected to present significant challenges for the ability of a 60/40 portfolio's potential to deliver results on par with previous levels, which is one factor driving more investors toward considering alternative investments.

We consider the macro environment prior to 2022 as the old regime and present a possible new regime, highlighting the case for alternatives.

Shifting from an old to new macroeconomic regime—the case for alternatives

| Old regime (~2012–2021) | New regime (2022–?) | The case for alternatives in a new regime |

| Accommodative global monetary policy promotes steady global economic growth | Increasingly restrictive global monetary policy results in a more defined economic cycle Geographical dispersions in economic growth rates and regular market dislocations |

Portfolio management may become more challenging as asset class and sector dislocations occur The environment may become more conducive to alpha generation inherent in many alternative strategies |

| Double-digit equity market returns in 8 out of 10 calendar years, according to Morningstar Direct | Moderate returns more consistent with long-term averages | Alternatives may be more attractive on a relative basis with greater opportunity to add value within portfolios |

| Persistently low volatility | Potentially higher volatility | Alternatives are needed more than ever to help reduce potential risk |

| Declining and persistently low interest rates | Increasing interest rates | Alternatives can offer diversification without duration risk |

| Consistently low inflation | Potentially higher and more uncertain inflation | Alternatives, such as real assets and private credit, help act as a potential inflation hedge |

| Bonds provided excellent portfolio diversification | Bonds' ability to diversify may be challenged | Alternatives tend to shoulder more of the diversification burden within portfolios |

This information may contain certain statements that may be deemed forward looking. No forecasts are guaranteed.

In a new regime, tailwinds of accommodative monetary policy may no longer exist. In this environment, we believe it’s reasonable to expect equity returns to be more moderate and consistent with long-term averages. Meanwhile, higher inflation and the removal of easy monetary policy are likely to result in greater market volatility and more pronounced business cycles. Importantly, in this environment, we believe risk-adjusted stock and bond returns may not be at historic highs, portfolios are harder to manage, and, therefore, a 60/40 portfolio faces a combination of challenges.

Where to from here?

Alternative strategies may add value to a diversified portfolio, providing investors access to differentiated return sources, potential downside protection, enhanced upside potential, and low correlation. While the past decade in particular has been favorable for equities and bonds with underlying performance drivers such as ultra-low interest rates, low inflation, low volatility, and quantitative easing, these factors have largely reversed. It stands to reason that in this new regime, alternatives can help to effectively address the challenges that traditional 60/40 portfolios may face; however, different types of alternatives can have meaningfully different risk/return characteristics, not only relative to each other, but also over time. As such, it's important for financial professionals to choose to partner with an investment firm that can provide asset allocation and portfolio construction support, as well as access to a diversified range of alternative solutions.

This article originally appeared in Why invest in alternative investments now by John P. Bryson, Head of Investment Consulting, and Michael L. Stephens, CFA, CAIA, Investment Consultant at John Hancock Investment Management.

1 Morningstar Direct, 2023.

2 Morningstar Direct, 2023. Long-term average measured over 60 years ending 2022.

3 Sharpe ratio is a measure of excess return per unit of risk, as defined by standard deviation. A higher Sharpe ratio suggests better risk-adjusted performance.

Important note:

The information provided on this website is for informational purposes only and is intended solely for use by Singapore residents and is not intended for distribution to, or use by, any person or entity in the United States, or any jurisdiction or country where such distribution or use would be contrary to law or regulation, or which would subject Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G), Manulife (Singapore) Pte. Ltd. (Company Registration No. 198002116D) and/or its affiliates (collectively hereafter "Manulife") or any of Manulife's products or services to any registration requirement within such jurisdiction or country. Nothing on this website shall be construed as financial advice or an offer, invitation, solicitation or recommendation by or on behalf of Manulife to any person to buy or sell any Fund and is no indication of trading intent in any Fund managed by Manulife. None of the information or analyses presented are intended to form the basis for any investment decision, and no specific recommendations are intended. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Thank you for contacting Manulife Singapore!

Our Financial Consultant will be in touch with you soon.

Here are some links you might find useful.

Consent

By submitting your personal details,

- You acknowledge that you authorise and consent to Manulife (Singapore) Pte Ltd ("Manulife) (including employees and Representatives of Manulife) to collect, use, disclose and retain your personal data for the purpose of receiving notifications via SMS(es) and email(s) to service your request; and

- You consent to Manulife to contact you (even though your telephone number may be already registered on the National Do Not Call Registry) for marketing purposes, and to provide you with marketing, advertising and promotional information, materials and/or documents relating to financial advisory services and products distributed by Manulife, if applicable.

The consent you provide is in addition to and does not supersede, vary or nullify any consent which you may have provided previously in respect of the above purposes, unless your previous consent has been withdrawn.

You also confirm that you are the user and/or subscriber of the telephone number and email address provided by you.

More Insights you might find interesting

What is an Investment-Linked Policy (ILP) and is it suitable for me?

How to invest your savings at every age.