A Complete Guide to Estate Planning

How to guarantee the continued well-being of your family and business after your passing.

26 October 2023 | 6-mins read

There's no greater indicator of success than the long-term wealth and well-being of one's family. To sustain your accomplishments far into the far future, it's imperative to plan for a time beyond your death.

What is Estate Planning?

Estate planning is the process of creating a strategy for the legal transfer of your assets to your heirs after your passing. To ensure everything goes according to your wishes, the plan should be based around a will, and might also include family trusts, life insurance, powers of attorney and business succession plans. The process is usually devised with the help of an estate-planning lawyer.

What Are the Benefits of Estate Planning?

Having a sound estate plan can help your heirs minimise legal costs, legwork and taxes. By thinking ahead, you can create equitable arrangements for asset distribution, helping to avoid future disputes and misunderstandings. Smart planning can also reduce how long it takes to transfer the money to your family, better provide for minors or dependents, and support your passion for charitable giving. It should also account for any outstanding debts (e.g. mortgages) to protect your spouse and children from undue burdens.

If you're an entrepreneur or executive who wants to safeguard the long-term fortunes of your businesses, estate planning presents a great opportunity to envision succession strategies for your companies.

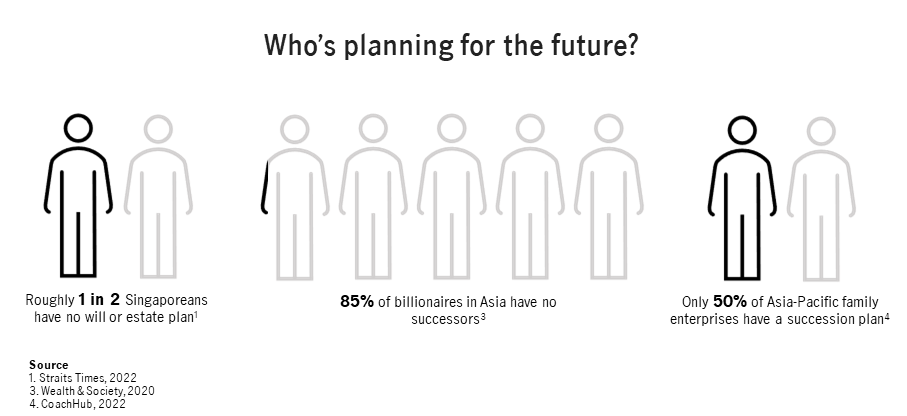

Yet, The Straits Times reports that in Singapore, 48% of respondents to a retirement and wealth planning survey have no will1. Other Asian countries have even lower rates of preparation. With an increasingly unstable world2 that weighs on economic fortunes worldwide, estate planning is supremely vital for protecting a family's future.

Creating Your Own Personal Estate Planning Strategy

'We have all heard of stories of families fighting over the assets of someone who has passed on. When the dispute goes to the court system, all parties lose because of the huge amount of acrimony involved – not to mention the costs. Rather than leave it to chance, do your estate planning early and spell out your wishes clearly so that they will be followed,' says Khoo Poh Huat, Chief Distribution Officer at Manulife Singapore.

Start your estate planning by creating a will. List your assets (cash, real estate, cars, personal property) and how you would like them distributed amongst your loved ones. Be specific to ensure your wishes are respected as best they can be. As you put together your will, consider how any debt will be paid. Remember to appoint an executor: someone you trust to carry out the directions in your will and legally administer your estate.

'Also think about how charity-giving fits into your estate plan,' says Khoo. 'If there are causes or pursuits that you are passionate about, it is worth thinking about how you might bequeath to them in your estate plan. And consider how tax will affect the transfer of wealth to your beneficiaries,' he adds. 'There are strategies to minimise the overall tax burden, so it is worth talking to a qualified financial advisor.'

You may also consider creating a living trust – the legal and organisational equivalent of a safe deposit box – for storing wealth. In some jurisdictions, this might allow descendants to avoid the time, cost or hassle of certain court proceedings; a family in mourning won’t want to handle legal complications.

A Step-by-Step Guide for Estate Planning

Estate planning extends beyond drafting a will. There are several practical concerns to keep in mind to ensure the timely and accurate distribution of your estate.

- Prepare a detailed inventory of financial assets and liabilities for your family. Include all outstanding debts and information on pensions and retirement benefits that survivors may be entitled to. Walk through all of your accounts with your heirs – bank accounts, credit cards, investment accounts, insurance policies, and loans etc. – along with contacts for each provider.

- Create a list of key contacts. These could include an attorney, accountant, financial consultantmand so on. Gather all the legal documents that your family may need to access and keep them in a safe place.

- Understand how your investments and savings accounts operate. Designate specific beneficiaries for each, so that any personal holdings transfer to the rightful heirs.

- Create an inventory of online accounts. These might include social media profiles, e-mails, bill payments – with the login and password details. Encrypt and password-protect this document.

- Keep your contact details up to date with financial providers. Regularly review your accounts to ensure outdated information (for example, an ex-spouse once included as a beneficiary) is revised.

- Monitor current or future liabilities. For instance, specify how to make outstanding mortgage payments and how your designated heirs should handle the ownership of associated assets.

- Start estate planning as early as possible. To save your family hiccups or hassles during a challenging period, include all the details of what you want to happen after your passing.

Make Diversifying Part of Your Plan

An indispensable component of estate planning is the optimisation of your investment portfolio. To give your family the best chances for success, it’s best to own a wide diversity of assets that’s resilient enough to last generations. By acquiring different asset types, you can hedge against economic downturns. With the advice of trusted financial professionals, build a broad basket of holdings that might include:

- Equities such as stocks. Stocks offer growth opportunities for investors, but be warned that they often come with higher risks and can underperform over time, causing more loss of investment than other assets.

- Fixed-income investments like bonds issued by governments and companies. These are generally favoured by investors with lower risk appetites, as they can help provide stability through recurring payments.

- Investment-linked policies (ILPs). These policies provide life-insurance coverage and investment components. The risk exposure is determined by which funds a holder chooses to invest in. Some of these options might pay potential dividends. Caveat: ILPs do not have any guaranteed cash value, so there’s a potential to lose the entire value of the investment.

- Real assets such as property and commodities. These deliver ongoing income and can safeguard against inflation.

- Alternative investments like private equity and hedge funds. Sometimes these options offer a notably high return.

- Real estate investment trusts (REITs). Buying into a REIT allows you to own a portion of a bundle of commercial and/or residential properties.

Ensure Business Continuity by Planning Your Company's Legacy

If you're a business owner, especially of a family-owned business, it's vital to engage in business-continuity planning. A central aspect of this planning is preparing for the unexpected loss of a 'keyman' – an individual responsible for much of the success and strategic capability of the organisation. These top decision makers are valuable corporate assets. The smaller and more tightly knit a firm is, the more substantial the risks associated with their departures. Unfortunately, research finds that many Asian businesses have inadequate business continuity plans in place5, underscoring the need for robust succession planning.

Your business continuity plan should outline the steps to take immediately after a keyman's passing or departure. To create this, you'll need to identify the areas of enterprise that will be affected, paying special attention to critical functions the company needs to survive. Then, map out the interdependencies between different departments. Losing a keyman in one department can often have far-reaching and unexpected effects on others. Finally, craft a strategy that includes built-in levels of redundancy to ensure the company operates normally, despite the difficult conditions. Be sure to have the technology, tools, people and systems in place to execute your plan.

A sound business-continuity plan should also include a disaster-recovery plan that calculates the potential time and cost of restoring normal operations after a natural disaster, political instability or a pandemic. Once built, test your business-continuity plan every three to six months to make sure it remains effective even as conditions change. Staff walkthroughs and table-top exercises can be a good way to assess your teams' preparedness. Over time, these activities will help you refine and improve the procedures, ensuring that your company's success will continue for years to come.

Top Tips for Business-Continuity Planning

- Identify the keymen in your business.

Who are the firm's controlling shareholders? Whose skills and insights would be difficult to replace? Which individuals are directly responsible for generating at least 5% of the company's profits? - Quantify the risks and costs associated with losing them.

What would it cost to replace these key personnel? How might their departure impact the firm's ability to succeed, both financially and in terms of opportunities and operations? - Implement risk-management measures.

Risk mitigation includes:- Purchasing universal life-insurance policies to cover the firm for any tragedy that befalls its key personnel.

- Having backup systems and procedures to help share the knowledge, relationships and know-how that key personnel possess, with other individuals in the business.

- Engaging in scenario planning and role-playing exercises with your staff that imagine the potential loss of key personnel and how they might respond to the challenges these losses present.

Start Your Plan for Tomorrow Today

Whether you are seeking to protect your family or your business after a death, the best plans are those thought-out well in advance – plans that are thorough, legally vetted and consider a host of scenarios that might threaten your intentions. It takes more than just wealth accumulation to create a legacy; it requires strategic forethought and a roadmap for the future that is adaptable and resilient.

Thank you for contacting Manulife Singapore!

Our Financial Consultant will be in touch with you soon.

Here are some links you might find useful.

Consent

By submitting your personal details,

- You acknowledge that you authorise and consent to Manulife (Singapore) Pte Ltd ("Manulife) (including employees and Representatives of Manulife) to collect, use, disclose and retain your personal data for the purpose of receiving notifications via SMS(es) and email(s) to service your request; and

- You consent to Manulife to contact you (even though your telephone number may be already registered on the National Do Not Call Registry) for marketing purposes, and to provide you with marketing, advertising and promotional information, materials and/or documents relating to financial advisory services and products distributed by Manulife, if applicable.

The consent you provide is in addition to and does not supersede, vary or nullify any consent which you may have provided previously in respect of the above purposes, unless your previous consent has been withdrawn.

You also confirm that you are the user and/or subscriber of the telephone number and email address provided by you.

Disclaimer

The information provided on this website is for informational purposes only and is intended solely for use by Singapore residents and is not intended for distribution to, or use by, any person or entity in the United States, or any jurisdiction or country where such distribution or use would be contrary to law or regulation, or which would subject Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G), Manulife (Singapore) Pte. Ltd. (Company Registration No. 198002116D) and/or its affiliates (collectively hereafter "Manulife") or any of Manulife's products or services to any registration requirement within such jurisdiction or country. Nothing on this website shall be construed as financial advice or an offer, invitation, solicitation or recommendation by or on behalf of Manulife to any person to buy or sell any Fund and is no indication of trading intent in any Fund managed by Manulife. None of the information or analyses presented are intended to form the basis for any investment decision, and no specific recommendations are intended. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Information correct as of 26 October 2023.

Sources

1 'Dying without a will: 48% of Singaporeans surveyed do not have one', 2022, BUSINESS, The Straits Times, https://www.straitstimes.com/business/invest/dying-without-a-will-48-of-singaporeans-surveyed-do-not-have-one

2 'Global Economic Uncertainty, Surging Amid War, May Slow Growth', 2022, Chart of the Week, IMF Blog, https://www.imf.org/en/Blogs/Articles/2022/04/15/global-economic-uncertainty-surging-amid-war-may-slow-growth

3 Peter Golovsky, 'Asian families must think beyond growth and overcome challenges in succession' 2020, Wealth & Society, https://www.wealthandsociety.com/updates-and-articles/asian-families-must-think-beyond-growth-and-overcome-challenges-in-succession

4 'Are Asian Businesses Equipped With Succession Plans?', 2022, CoachHub, https://www.coachhub.com/en/blog/are-asian-businesses-equipped-with-succession-plans/

5 'Succession Planning Report 2019', 2019, Asian Private Banker, https://asianprivatebanker.com/research/succession-planning-report-2019/

More Insights you might find interesting

How to invest your savings at every age.

What is an Investment-Linked Policy (ILP) and is it suitable for me?