The Manulife Asia Care Survey 2024 shows how people across Asia perceive their current and future physical, mental, and financial well-being, and how Manulife can be their partner for progress. Manulife surveyed more than 1,000 Singapore respondents in January 2024.

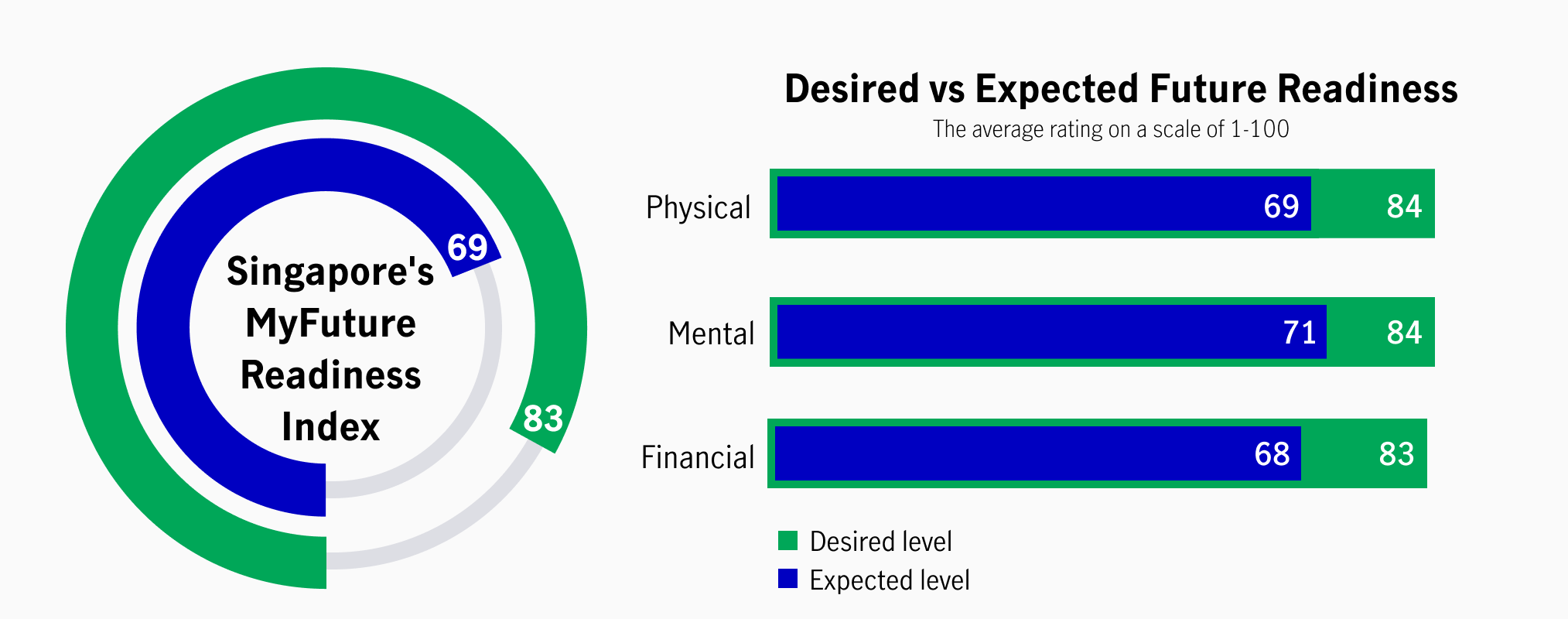

Singapore respondents have high aspirations for their future physical, mental, and financial well-being but they are unsure if they will achieve their desired levels of well-being.

They feel most unprepared for their 'financial' well-being in ten years, with 14 points' difference between their 'desired' and 'expected' future well-being.

Singapore respondents also rank mental well-being as the most important and financial well-being as the least important. In fact, mental well-being, physical health, and future health indicators are equally important, as mental health can also serve as a sign for future physical ailments.

Let's take a deeper look at what challenges they are facing:

What problems will Singaporean face?

These are the top 3 financial goals of Singaporeans

The top three long-term financial goals Singaporeans want to achieve are having enough savings for emergencies, having sufficient funds for their healthcare or medical needs, and enjoying financial freedom or security after retirement.

Over 80% thinks that the financial threat comes from rising healthcare costs

Singaporeans are most concerned about rising healthcare and living costs. At regional level, people believed that healthcare costs have increased by more than 20% in the past 12 months. This leads to the huge gap between their future expected and desired financial well-being.

At the same time, with the rising cost of living eroding people's purchasing power and reducing disposable incomes, Singaporean perceive the highest inflation rate in grocery costs and eating out spending.

In response, over 56% chose to reduce their non-essential spending, instead of reducing their investment and insurance expenses.

73% of respondents agree that even in an inflationary environment like now, insurance is still essential and necessary. 75% agree it is important that their insurance policy coverage and benefits keep up with the rising costs of living.

How will people achieve their financial goals under inflation?

Cash is still king when inflation bites

Nearly 70% of respondents rely on cash savings and bank deposits rather than other investment tools to achieve their goals.

Over 50% of respondents are reducing non-essential spending to shield themselves from inflation

Cuts in daily life spending |

56% Reduced spending on non-essential items |

55% Cut back on dining-out expenses |

41% Reduced the amount of entertainment activities |

34% Lowered consumption of luxury products or services |

Cuts in investment and insurance spending |

14% Reduced investment in different financial products |

13% Cut or reduced my own insurance expenses |

10% Cut or reduced my family's insurance expenses |