This content was contributed by Manulife Investment Management (Singapore) Pte. Ltd

Plan for retirement with inflation in mind

07 September 2021 | 2-mins read

How much savings do you think is sufficient for retirement? S$1 million? S$2 million? To live comfortably in your silver age, your goal should not be merely to accumulate assets worth a nominal value. Inflation should also be considered to ensure an investment appreciates over the years, so its real purchasing power can satisfy your retirement needs. If an investment strategy is too conservative, the principal could be preserved at retirement, but its purchasing power may be eroded by inflation.

The destructive effects of inflation should not be underestimated, as even a slight increase (which compounded over the years) can lead to a heavy burden in retirement. However, its actual impact depends on changes in expected inflation and age. In simple terms, younger people are affected more because they are further away from retirement age, which means high inflation erodes their purchasing power over a longer period.

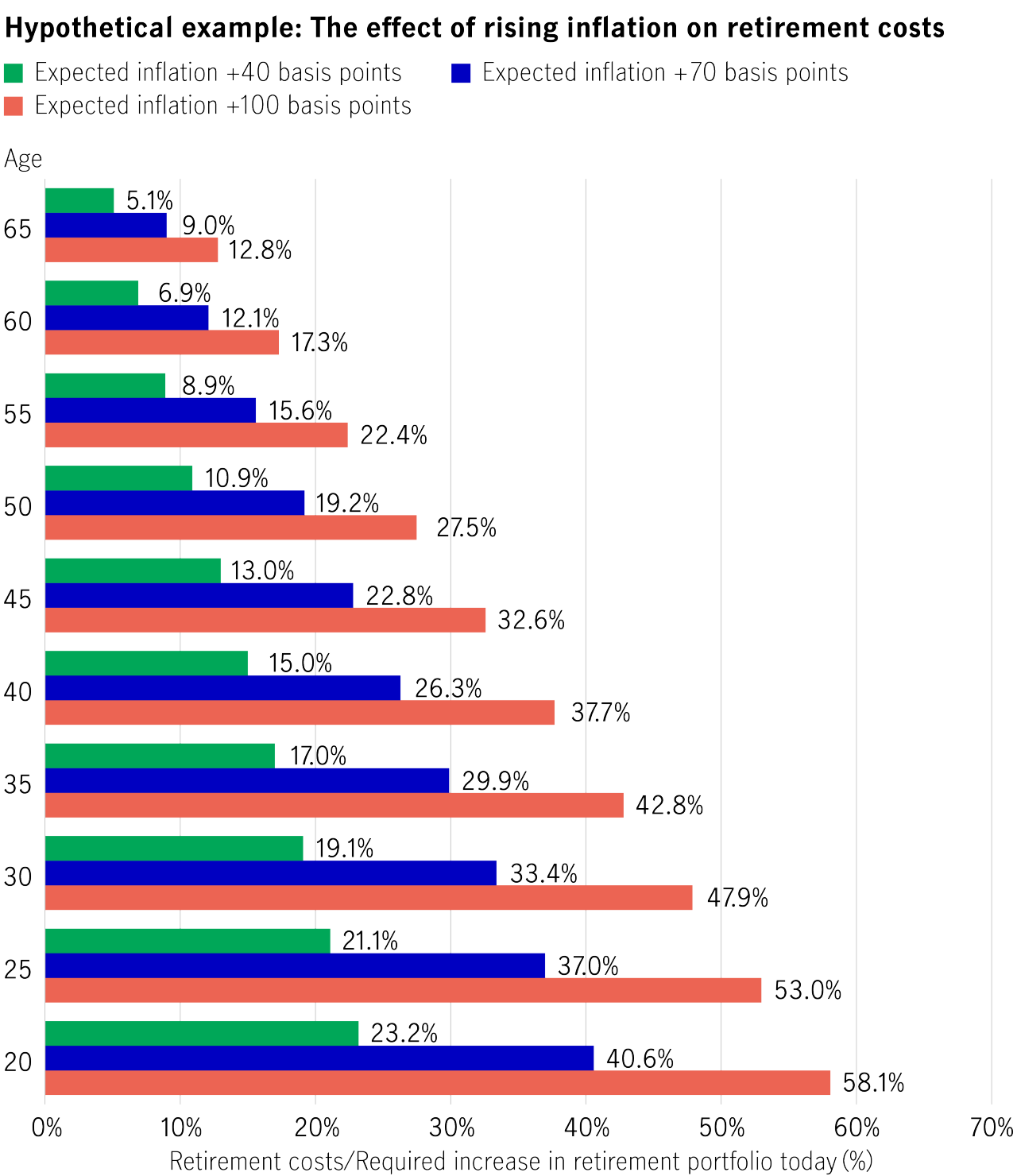

According to Manulife Investment Management’s calculations, suppose there are three investors aged 25, 45, and 65, respectively, who all retire at age 65 and have the same annual expected expenses after retirement. We found that:

- A 40 basis points (bps) increase in expected inflation will result in a 21.1%, 13.0%, and 5.1% increase in retirement costs, respectively.

- If expected inflation increases to 100 bps, retirement costs will increase by 53.0%, 32.6%, and 12.8%,1 respectively.

Looking at it from another perspective, the three individuals must immediately increase the corresponding amount of savings/wealth in their retirement portfolios (i.e., increase their savings) to offset the effects of inflation so that they can withdraw the predetermined amount of real income (i.e., inflation adjusted) each year according to plan.

Manulife Investment Management calculations, as of 1 February 2022.

Manulife Investment Management calculations, as of 1 February 2022.

It is, of course, not easy to inject a large lump sum into your retirement portfolio. If investors do not have spare or ready cash or choose to ignore inflation, the purchasing power of their assets will be heavily discounted in the future.

For example, if price levels rise at 2% per year, and the investment return is assumed to be 0% (holding cash and not making investments) and 1% (lower risk assets with an annual return lower than inflation) each year, real purchasing power (inflation-adjusted purchasing power of assets) after 35 years will be 50% and 29% less, respectively!

If the investment return rises to 2% each year, which is equal to the inflation rate, real purchasing power will remain the same throughout the investment period until retirement. Suppose the expected investment return rises further to 5% each year – in that case, your real purchasing power will increase continuously as the return is higher than inflation, and you will have gained 176% by retirement (see the following hypothetical example).

Hypothetical example: The effect of rising inflation on purchasing power

Assumptions:

- In 2022, an investor at age 30 has S$100,000 of assets and plans to retire 35 years later in 2057.

- In the same year, the price of daily necessities is S$100, and 1,000 units can be purchased with the assets held.

- The price of daily necessities (inflation) increases by 2% each year.

- There are four proposed retirement portfolios, with an annual expected return of 0%, 1%, 2%, and 5%, respectively.

Example for illustration only.

Example for illustration only.

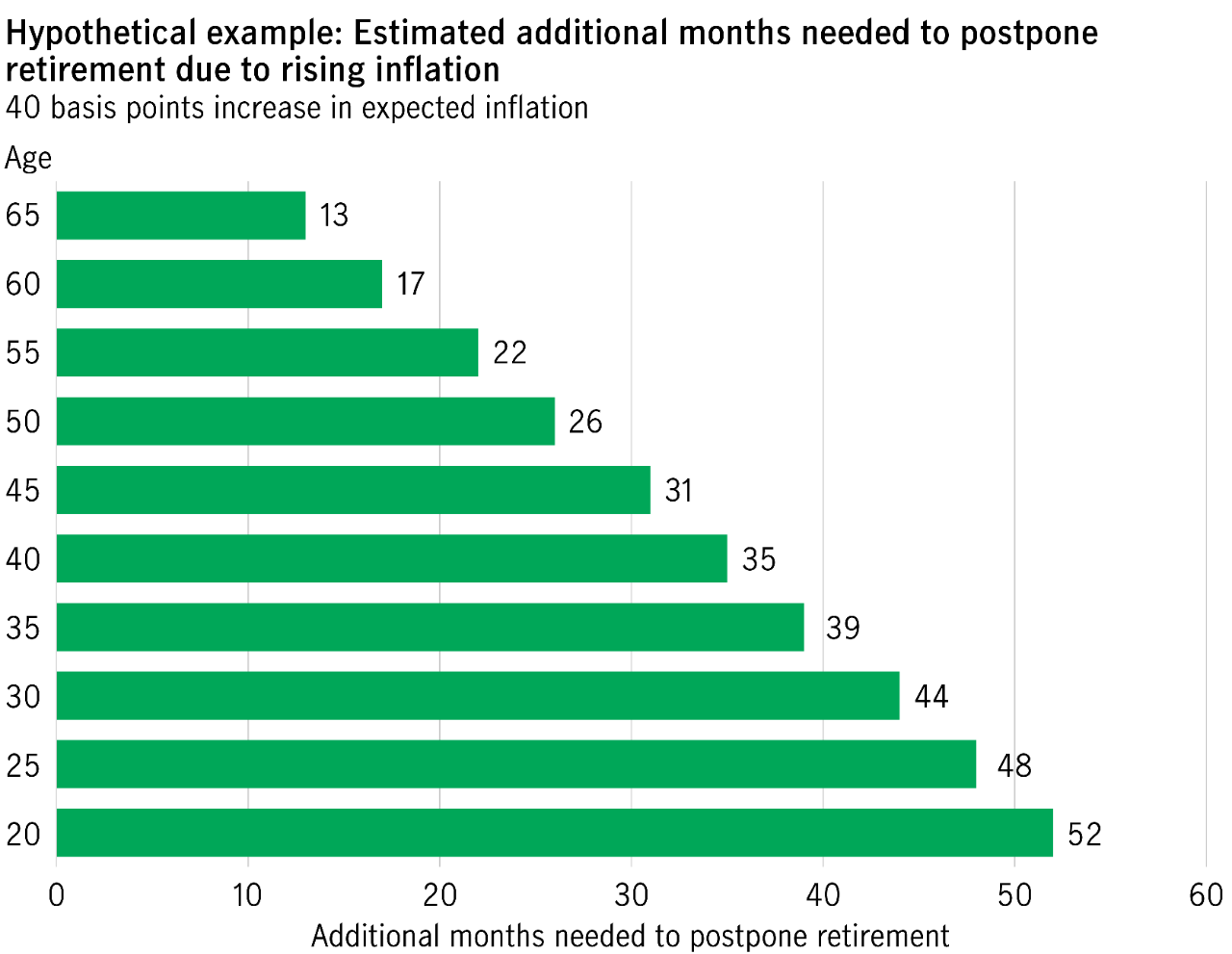

With inflation on the rise, if investors cannot inject more savings/funds into their portfolios but wish to avoid eroding their real purchasing power, they can consider postponing retirement.

Manulife Investment Management calculations, as of February 1, 2022.

Manulife Investment Management calculations, as of February 1, 2022.

In the example above, if expected inflation rises by 40 bps, investors at ages 25, 45, and 65 would have to postpone retirement by 48, 31, and 13 months, respectively, to accumulate enough savings to cover their post-retirement expenses.

Conclusion

No one can control the rise and fall of inflation or accurately predict how prices will rise in the future. Investors should understand the effects of rising inflation on retirement costs and plan according to the above examples. Therefore, it is crucial to consider inflation when planning for retirement. The growing rate of an investment portfolio (portfolio return) should keep up with or even exceed inflation. As young investors will not be retiring soon, they can tolerate a higher level of risk. Therefore, their portfolios may focus on assets with a greater potential return, such as equity funds and bond funds.

1. Manulife Investment Management calculations, as of 1 February 2022. This is a hypothetical mathematical illustration only. This is under certain assumptions about real interest rates and asset class returns of the multi-asset solutions team. Figures are based on assumptions as set out, and individual circumstances and objectives may vary.

Important note:

The information provided on this website is for informational purposes only and is intended solely for use by Singapore residents and is not intended for distribution to, or use by, any person or entity in the United States, or any jurisdiction or country where such distribution or use would be contrary to law or regulation, or which would subject Manulife Investment Management (Singapore) Pte. Ltd. (Company Registration No. 200709952G), Manulife (Singapore) Pte. Ltd. (Company Registration No. 198002116D) and/or its affiliates (collectively hereafter "Manulife") or any of Manulife's products or services to any registration requirement within such jurisdiction or country. Nothing on this website shall be construed as financial advice or an offer, invitation, solicitation or recommendation by or on behalf of Manulife to any person to buy or sell any Fund and is no indication of trading intent in any Fund managed by Manulife. None of the information or analyses presented are intended to form the basis for any investment decision, and no specific recommendations are intended. This advertisement has not been reviewed by the Monetary Authority of Singapore.

Thank you for contacting Manulife Singapore!

Our Financial Consultant will be in touch with you soon.

Here are some links you might find useful.

Consent

By submitting your personal details,

- You acknowledge that you authorise and consent to Manulife (Singapore) Pte Ltd ("Manulife) (including employees and Representatives of Manulife) to collect, use, disclose and retain your personal data for the purpose of receiving notifications via SMS(es) and email(s) to service your request; and

- You consent to Manulife to contact you (even though your telephone number may be already registered on the National Do Not Call Registry) for marketing purposes, and to provide you with marketing, advertising and promotional information, materials and/or documents relating to financial advisory services and products distributed by Manulife, if applicable.

The consent you provide is in addition to and does not supersede, vary or nullify any consent which you may have provided previously in respect of the above purposes, unless your previous consent has been withdrawn.

You also confirm that you are the user and/or subscriber of the telephone number and email address provided by you.

More Insights you might find interesting

5 tips to know for retirement planning

Guide to retirement planning for young adults