How Much Insurance Coverage Do You Need for Common Types of Critical Illnesses in Singapore?

20 February 2024 | 8-mins read

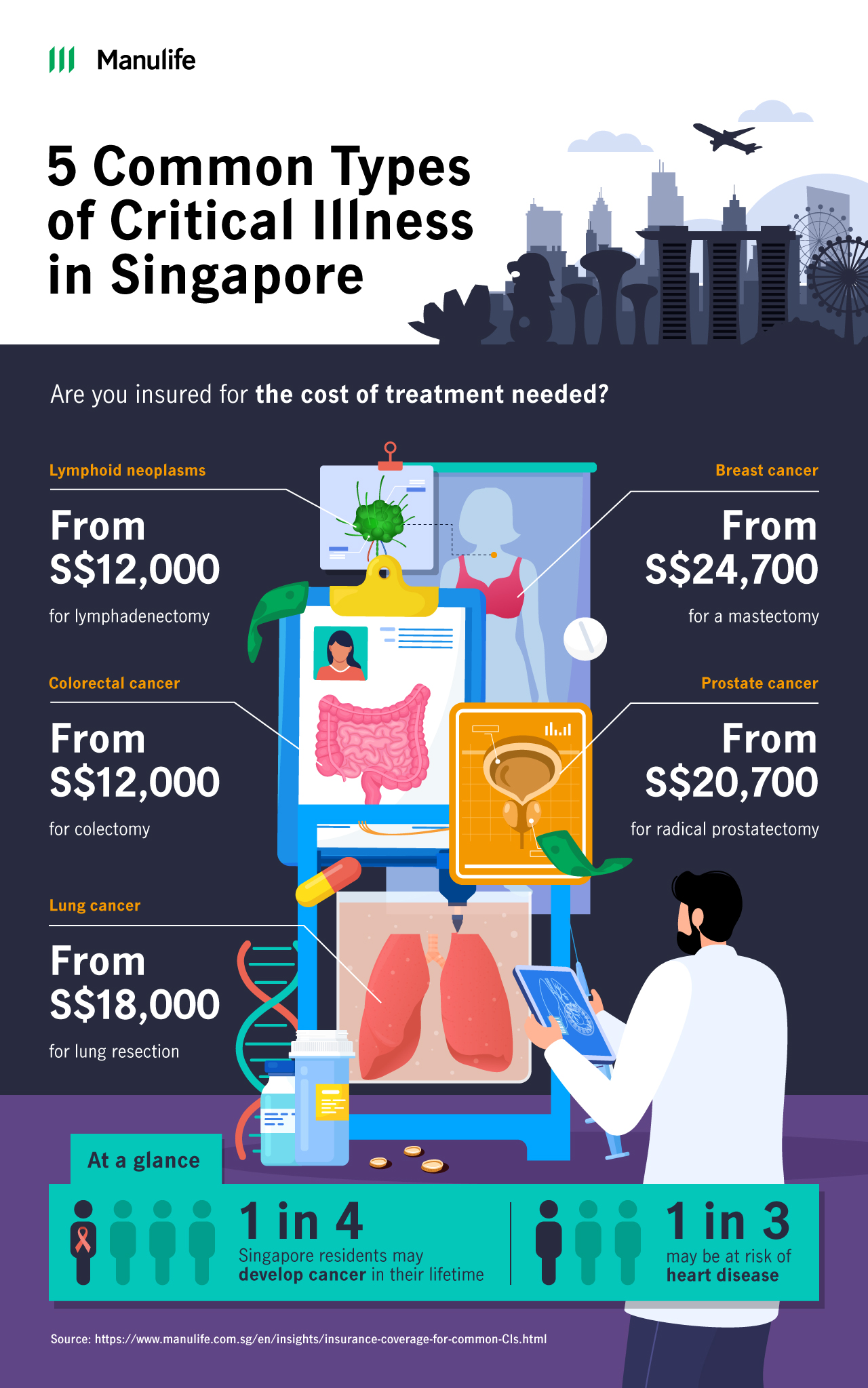

As the life expectancy of Singapore's residents increases1, so too does the risk of developing a critical illness. A study shows that about one in four2 Singaporean residents may develop cancer during their lifetime, while one in three3 may be at risk for underlying cardiovascular diseases such as heart disease.

According to the Ministry of Health's (MOH) fee benchmarks for operations4, critical illness procedures such as open chest heart valve surgery can easily cost S$30,000 or more. This is why it is crucial to have adequate critical illness insurance to safeguard yourself and your loved ones from the financial burden of medical bills and loss of income.

What are the most common types of critical illness in Singapore?

As defined by the Life Insurance Association Singapore (LIA)5, critical illness insurance is a type of policy that provides financial protection if you are diagnosed with a major illness and ensures that you and your family's needs are met during the recovery period. Here are the five most common types of critical illnesses and their respective treatment costs based on statistics from the Singapore Cancer Society6 and the Ministry of Health's List of Fee Benchmarks4:

- Breast cancer: is the most common cancer among women in Singapore (12,735 cases in the period of 2017-202113), with the cost of a mastectomy ranging from S$24,700 to S$35,000.

- Colorectal cancer: affects both men (6,697) and women (5,542), with the cost of colectomy surgery ranging from S$12,000 to S$18,000.

- Lung cancer: is prevalent in both men (5,567) and women (3,388), with the cost of lung resection surgery ranging from S$18,000 to S$28,000.

- Prostate cancer: is the leading cancer among men (6,912 cases), with the cost of radical prostatectomy surgery ranging from S$20,700 to S$27,200.

- Lymphoid neoplasms: are types of malignant cancers like lymphoma that affect both men (2,986) and women (2,221), with the cost of lymphadenectomy surgery ranging from S$12,000 to more than S$20,000 depending on the complexity of the procedure.

Many risk factors can cause the illnesses mentioned above. These can include genetics, smoking, UV exposure, radiation exposure, and previous cancer treatments such as chemotherapy and radiotherapy.

While cancer makes up some of the most common critical illnesses, cardiovascular conditions such as heart disease are another major health concern as they can lead to heart attacks, coronary artery disease, and heart valve problems.

The treatment of these conditions may require coronary bypass surgery or pacemakers, which are costly procedures. According to the Singapore Heart Foundation, cardiovascular disease is also the leading cause of death in Singapore, accounting for 31.4% of deaths as of 2022.

The LIA lists 37 standard critical illnesses covered by insurers7 includes, but is not limited to:

- Major cancer (e.g. leukaemia, lymphoma, sarcoma, etc.)

- Heart attack of specified severity

- End-stage kidney failure

- End-stage liver failure

- Major burns

- Major organ/bone marrow transplants

- Benign Brain Tumour

- Blindness (irreversible loss of sight)

- Terminal illness

- Paralysis (irreversible loss of use of limbs)

The importance of early detection and critical illness insurance

Health screenings are crucial for detecting the early signs of cancer before symptoms appear, which can lead to more effective treatment and lower costs. Regular health screenings are recommended8 as symptoms may not appear for early-stage cancers, and the treatment for early stages is typically less invasive than more advanced ones.

Critical illness insurance provides a lump sum payout if you are diagnosed with a serious medical condition that is covered by the policy, such as cancer or cardiovascular disease. This payout can be used to help cover medical and daily living expenses.

It is worth noting that most of the critical illness policies generally cover only advanced stages of cancer. However, some policies are available that cover early-stage cancer9 and provide a payout to help cover medical fees and living expenses.

How much critical illness insurance coverage do you need?

Skipping critical illness insurance could be a big mistake10, as it only takes one critical illness diagnosis to create a sizable financial burden for you and your family. In the event of critical illness, you may face medical expenses, rehabilitation costs, and the loss of income. If you are unprepared, this situation can rapidly deplete your savings, leading to major lifestyle changes to manage your family's living expenses.

That is why it is important to have critical illness protection to cover medical treatments and make up for lost income, so you can ease the financial burden on your family.

According to the Life Insurance Association Singapore's (LIA) 2022 Protection Gap Study11, you need approximately 4x your annual income for adequate critical illness insurance coverage. This number is based on an assumed critical illness recovery period of five years before an insured can return to workforce.

So if you earn S$72,000 a year, you'll need at least S$288,000 in critical illness coverage. This should help ensure you have enough financial protection in case a critical illness prevents you from working for an extended period of time.

While having 4x your annual income is a general guideline, you will need to determine the right level of insurance coverage for your own unique situation based on factors such as your income, savings, financial responsibilities, and health conditions.

Understanding the critical illness insurance "protection gap"

Most Singapore residents have a "critical illness insurance protection gap" when it comes to critical illness coverage. This means the coverage you have may not be enough to pay for the total cost of treatment and recovery if you are diagnosed with a critical illness. The critical illness protection gap refers to the difference between the coverage you need and the coverage you actually have.

According to the LIA, economically active Singapore residents – employed individuals who are contributing to the production and distribution of goods and service – have a 74% critical illness protection gap. In other words, in the event of a critical illness diagnosis, the average economically active Singapore resident would only have enough insurance protection to cover 26% of the total cost of medical expenses, treatments, and loss of income.

To put this into perspective, let us calculate the critical illness insurance protection you need using this simple formula:

Critical illness protection goal – Available resources = Critical illness protection insurance gap

[Your annual income x 4] – [Existing critical illness insurance coverage + Savings] = Critical illness protection gap

Let us look at your critical illness insurance protection gap if your annual salary is S$60,000, your existing critical illness insurance coverage is S$100,000, and your savings is S$50,000.

Critical illness protection goal – Available resources = Critical illness protection insurance gap

S$24,000 (S$60,000 x 4) – S$150,000 (S$100,000 + S$50,000) = S$90,000 (37.5%)

Based on the example above, your critical illness insurance protection gap would be S$90,000, or 37.5%.

Illustrating the impact of the critical illness insurance protection gap

To illustrate the importance of bridging the critical illness insurance protection gap, let us look at a simple example.

Sabrina, a 35-year-old, earns a yearly salary of S$66,000. She also has an existing critical illness coverage of S$50,000 and has built up S$80,000 in savings. She believes that she is in reasonably good health and has adequate insurance protection against any health crises.

Based on her existing coverage and savings, she has a critical illness insurance protection gap of S$134,000, or 50.8%.

Critical illness protection goal – Available resources = Critical illness protection insurance gap

S$264,000 (S$66,000 x 4) – S$130,000 (S$80,000 + S$50,000) = S$134,000 (50.8%)

Over time, she begins to feel a growing body pain and discomfort and decides to see a doctor. After tests are run, she is diagnosed with a late-stage critical illness. The cost of surgery and chemotherapy amounts to an estimated cost of S$200,000. She is expected to need at least 6 months to recover, during which she will lose some income as she is only entitled to 60 days of paid hospitalisation leave12.

As her available resources from her lump sum critical illness policy payout and savings are only S$130,000, she has a shortfall of S$70,000 in paying off her medical costs of S$200,000. However, if she had fully maximised her critical illness protection goal of S$264,000, she would have had enough from her lump sum payment alone to manage her medical costs without using her hard-earned savings.

The importance of having a critical illness policy with enough coverage

To ensure you have enough protection in case of a critical illness diagnosis, there are a few key details you should take note of:

Understand the benefits and limitations of critical illness insurance

A critical illness policy can provide a lump sum payout upon diagnosis of the covered critical illnesses that can help cover medical and daily living expenses during the recovery period when you may have a loss of income. The recovery period may range from a few months to a few years, depending on the critical illness. According to the LIA's 2022 Protection Gap Study, you should have enough critical illness insurance coverage to cover a benchmark recovery period of five years11. However, critical illness policies do have their limitations.

Generally, these policies only cover a specific list of illnesses7, and may not cover others. Additionally, some policies may only cover advanced stage cancer, which means you may not be able to cover treatment unless you have a policy that covers early-stage cancer.

Premiums may also be high for adequate coverage, and there may be a waiting period before the policy goes into effect.

Choose the right critical illness insurance plan for your needs

Critical illness policies can come as either standalone policies or as a rider to your existing health insurance plan. Some riders can cover conditions like early-stage critical illnesses or disability, and even provide additional cash payouts for less severe diagnoses.

When choosing a critical illness policy, always confirm what medical conditions it covers, the terms and conditions to claim for each medical condition, and how flexible it is in covering evolving medical needs such as early- to late-stage cancers. You should aim for sufficient coverage to eliminate critical illness protection gap and consider a policy that offer the option to renew.

Make lifestyle changes and go for regular health screenings

While a healthy lifestyle does not guarantee that you will never be diagnosed with a critical illness, it can help reduce the risks. This means exercising regularly, eating a balanced diet, limiting alcohol consumption, and avoiding smoking.

Regular health screenings and check-ups can also help detect critical illnesses early when they may be more treatable and less costly, as expensive treatments and procedures may not be necessary.

Taking steps to buy adequate critical illness insurance coverage and focusing on preventive health measures will give you peace of mind knowing you have enough protection if you receive a serious medical diagnosis.

Safeguarding your financial future with adequate critical illness coverage

Having a critical illness insurance policy with adequate coverage is extremely important for your health and finances. As a young working adult in Singapore, a critical illness diagnosis can easily derail your life plans and drain your savings quickly.

The financial costs of critical illnesses highlight why having enough insurance coverage to bridge the critical illness protection gap is so important.

Speak to a financial consultant to review your existing insurance coverages, understand new critical illness policies and riders and find one with coverage that will provide the protection you need if you are diagnosed with critical illness. By taking action today, you can have peace of mind knowing that you and your loved ones are protected against the financial burden of the hefty medical expenses and loss of income.

Thank you for contacting Manulife Singapore!

Our Financial Consultant will be in touch with you soon.

Here are some links you might find useful.

Consent

By submitting your personal details,

- You acknowledge that you authorise and consent to Manulife (Singapore) Pte Ltd ("Manulife) (including employees and Representatives of Manulife) to collect, use, disclose and retain your personal data for the purpose of receiving notifications via SMS(es) and email(s) to service your request; and

- You consent to Manulife to contact you (even though your telephone number may be already registered on the National Do Not Call Registry) for marketing purposes, and to provide you with marketing, advertising and promotional information, materials and/or documents relating to financial advisory services and products distributed by Manulife, if applicable.

The consent you provide is in addition to and does not supersede, vary or nullify any consent which you may have provided previously in respect of the above purposes, unless your previous consent has been withdrawn.

You also confirm that you are the user and/or subscriber of the telephone number and email address provided by you.

Footnotes

- https://www.singstat.gov.sg/-/media/files/publications/population/lifetable21-22.ashx

- https://www.singaporecancersociety.org.sg/learn-about-cancer/cancer-basics/common-types-of-cancer-in-singapore.html

- https://www.straitstimes.com/singapore/health/launch-of-nationwide-preventive-heart-health-study-to-help-pick-up-hidden-diseases#:~:text=Heart%20disease%20is%20a%20top,heart%20disease%20that%20remains%20undetected.

- https://www.moh.gov.sg/docs/librariesprovider5/default-document-library/full-list-of-fee-benchmarks_230615-(2).pdf

- https://www.lia.org.sg/media/2272/be-in-the-know-about-critical-illness-plans.pdf

- https://www.singaporecancersociety.org.sg/learn-about-cancer/cancer-basics/common-types-of-cancer-in-singapore.html

- https://www.lia.org.sg/media/2160/mu5819-part-2-of-4-_lia-ci-framework-2019_lia-definitions-for-37-cis.pdf

- https://www.singaporecancersociety.org.sg/get-screened/why-go-for-regular-cancer-screening.html

- https://www.manulife.com.sg/en/insights/do-i-need-an-early-stage-critical-illness-plan.html

- https://www.manulife.com.sg/en/insights/5-reasons-why-critical-illness-insurance-matters.html

- https://www.lia.org.sg/media/3976/lia-pgs-2022-key-findings_final-8-sep-2023.pdf

- https://www.mom.gov.sg/employment-practices/leave/sick-leave/eligibility-and-entitlement

- https://www.nccs.com.sg/patient-care/cancer-types/cancer-statistics#:~:text=Cancer%20Incidence%20in%20Singapore&text=Females%3A%20breast%20(12%2C735%20cases%2F,(3%2C388%20cases%2F7.9%25).

More Insights you might find interesting

Debunking critical illness myths

How is Critical Illness Plan different from Health Insurance?